Understanding the difference between independent contractors and employees is crucial for more than just compliance—it impacts tax responsibilities, payroll processes, and financial planning. Employers are required to withhold taxes like Social Security and Medicare for employees, but not for independent contractors. Misclassifying workers can lead to costly penalties, so it’s essential to get it right. This guide provides clear, practical tips to help you confidently classify roles and avoid common mistakes.

Key Differences Between an Independent Contractor and an Employee

Misclassifying workers can lead to expensive penalties and legal issues, so it’s critical to understand the differences between independent contractors and employees. These distinctions focus on control, work structure, tax responsibilities, and more. Below, we break it down in detail, helping you make informed decisions.

Hiring Practices

Hiring employees and independent contractors follows very different processes.

Employees are hired through formal job applications, often managed by HR. They go through interviews, agree on benefits and salaries, and become part of the organization’s structure.

Independent contractors, on the other hand, negotiate directly with project managers. They submit proposals outlining their rates and methods, and their contracts end when the project is complete.

Control Over Work

The level of control a business has over a worker’s tasks is one of the clearest indicators of classification.

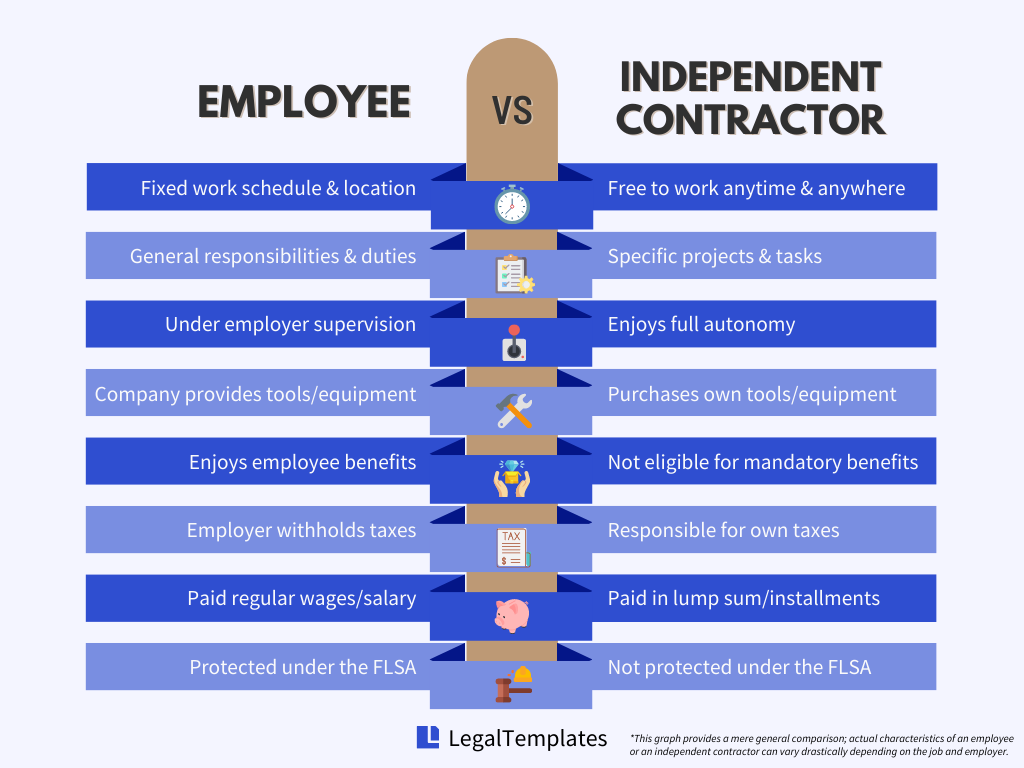

Employees follow company schedules, workflows, and protocols. Employers dictate their hours, location, and methods for completing tasks. Employers frequently use employee monitoring software to track productivity and guarantee adherence to company standards.

Independent contractors have autonomy. They choose their schedule, tools, and processes as long as they meet deadlines.

Example

An employee works 9–5 at the office using company-provided tools. A contractor, hired to build a website, works remotely and determines their own work hours.

If you’re directing how someone does their work, they’re likely an employee, not a contractor.

Work Location

Where work is performed can also help determine worker status.

Employees typically work at a specific location chosen by the employer, such as an office or designated remote setup.

Independent contractors decide where they work—whether at home, a coworking space, or the client’s site—based on project needs.

Example

A full-time IT support employee works at the company office, while a freelance cybersecurity expert performs tasks remotely.

Payment and Taxes

Payment structures and tax responsibilities vary significantly. Employees have taxes withheld by their employer and receive a W-2 form for tax reporting. Independent contractors manage their own taxes and receive a 1099-NEC form for payments exceeding $600. There are key differences between 1099 and W-2 forms you should know.

| Aspect | Employees | Contractors |

|---|---|---|

| Payment | Fixed salary or hourly | Paid per project/milestone |

| Taxes | Employer withholds taxes | Pay own self-employment |

| Tax Reporting | W-2 filed by employer | Receive 1099-NEC form |

IMPORTANT: Tax Forms

Businesses must file Form 1099-NEC for payments to contractors exceeding $600 in a year. Employees receive Form W-2 for tax reporting.

Training and Development

Companies often train employees, while contractors are expected to bring expertise to the table.

Employees receive on-the-job training, and employers may cover external learning opportunities to improve skills.

Independent contractors invest in their own development and are hired because of their existing qualifications and knowledge.

Avoid extensive training for contractors, as significant guidance could legally classify them as employees.

Benefits and Incentives

Benefits are a key feature of employee relationships. Employees often receive perks such as health insurance, retirement plans, paid leave, and bonuses, which employers may be required to provide by law. Employers also frequently reimburse employees for work-related expenses, such as travel or supplies.

Independent contractors, on the other hand, do not receive benefits or reimbursements. Instead, they set their rates to account for expenses like health insurance, retirement savings, and other operating costs they cover themselves.

Duration of Work

The nature and length of the work relationship often determine worker status.

Employees are typically hired indefinitely as part of the company’s long-term structure.

Independent contractors are brought in for specific, short-term projects. Contracts define the start and end of the working relationship.

Example

A marketing employee works year-round. A freelance photographer is hired for a one-time product photoshoot.

Performance, Termination, and Compliance

Performance expectations, termination procedures, and adherence to industry standards often differ between employees and independent contractors.

Performance

Employees are subject to ongoing performance evaluations and must meet company-defined goals and standards. Independent contractors are judged on deliverables outlined in their contracts, with success measured by completed tasks rather than ongoing reviews.

Termination

Employees are typically protected by labor laws and may require formal notice or severance when terminated. In contrast, contractors can usually be released at the end of a project or per contract terms, often with fewer legal requirements.

Compliance

Employers ensure employees adhere to company policies and industry regulations. Contractors are expected to follow applicable laws and standards within their field but are responsible for their own compliance, such as maintaining licenses or certifications.

Financial Investment, Risk, and Liability

Employees rely on their employer to provide the tools and resources needed for their work, with no financial risk or liability. Employers are responsible for their employees’ actions within the scope of their job duties.

Independent contractors, however, invest in their own tools, software, and equipment. They bear the financial risks of their business and may also be subject to indemnification clauses, making them accountable for issues arising from their work.

Example

An employer provides laptops to employees and takes on liability for their actions. A contractor purchases specialized software and assumes responsibility for its use and outcomes.

Confidential Information and Trade Secrets

The handling of confidential information and trade secrets differs between employees and independent contractors.

Employees typically sign confidentiality agreements as part of their employment, ensuring trade secrets and proprietary information remain protected.

Independent contractors, while often signing similar agreements, work outside the company’s structure. Specific contract terms are essential to safeguard sensitive information, especially as contractors may work with multiple clients.

Example

An employee signs a company-wide NDA during onboarding. A contractor signs a project-specific agreement to protect client data.

| Aspect | Employees | Contractors |

|---|---|---|

| Employment Laws | Covered by FLSA, etc. | Not covered by laws |

| Unemployment | Eligible for benefits | Not eligible |

| Overtime | Entitled under FLSA | Not entitled |

Consult legal professionals to ensure workers are properly classified and receive the protections they’re entitled to.

Contractor vs. Freelancer (vs. Employee)

Choosing the right type of worker for your business can feel confusing. Contractors, freelancers, and employees each bring something different to the table. Here’s how they compare so you can confidently make the right decision.

Contractor vs Freelancer

Both contractors and freelancers work independently, but they differ in their commitment and work scope.

Contractors focus on long-term projects or well-defined deliverables. They typically work under formal agreements with set timelines.

Freelancers are often hired for short-term, flexible tasks. They work with multiple clients, managing smaller projects as needed.

Choose contractors for big projects with clear timelines, and freelancers for quick, creative tasks.

Example

A graphic designer hired for a single logo design is a freelancer. A contractor, however, might handle your full rebranding campaign over several months.

Freelancer vs Employee

Freelancers and employees work very differently. Understanding their distinctions helps you avoid costly misclassifications.

| Aspect | Freelancer | Employee |

|---|---|---|

| Control | Sets their own schedule | Follows employer’s hours |

| Pay | Paid per project or invoice | Regular salary or wage |

| Benefits | No benefits provided | Health, PTO, retirement |

| Work Relationship | Short-term, flexible | Ongoing, long-term |

Key Difference: Freelancers operate with full independence, managing their time and projects. Employees work under employer direction and receive workplace benefits.

If you require someone to follow a set schedule or use your tools, they likely qualify as an employee—not a freelancer.

Why Proper Classification Matters

Correctly classifying workers as independent contractors or employees isn’t just about compliance—it protects your business financially and builds trust within your workforce. Understanding the risks of misclassification helps you avoid costly mistakes.

Legal Consequences

Misclassifying workers can violate employment laws, leading to penalties and audits.

Agencies like the IRS and Department of Labor ensure worker classifications align with tax and employment laws.

Example

If a worker is misclassified, employers may owe unpaid wages, penalties, and overtime under the Fair Labor Standards Act (FLSA).

Financial Risks

Misclassification can lead to unexpected costs that impact your business’s finances:

- Back taxes: Repay Social Security, Medicare, and unemployment taxes.

- Penalties: Cover fees for late or incorrect filings.

- Unpaid wages: Pay owed overtime, benefits, or wages to misclassified workers.

Accurate classification saves you from costly corrections later.

Reputational Impact

Worker misclassification can damage your company’s relationships and public image:

- Employee trust: Misclassified workers may feel undervalued.

- Client confidence: Compliance issues can raise red flags for partners.

- Company reputation: Legal or financial penalties may attract negative publicity.

Classify workers accurately from the start to strengthen trust and avoid reputational risks.

How to Classify Workers

Classifying workers correctly as employees or independent contractors is key to staying compliant with labor and tax laws. To simplify this process, the US Department of Labor and IRS use guidelines to help you assess worker relationships. Here’s what you need to know.

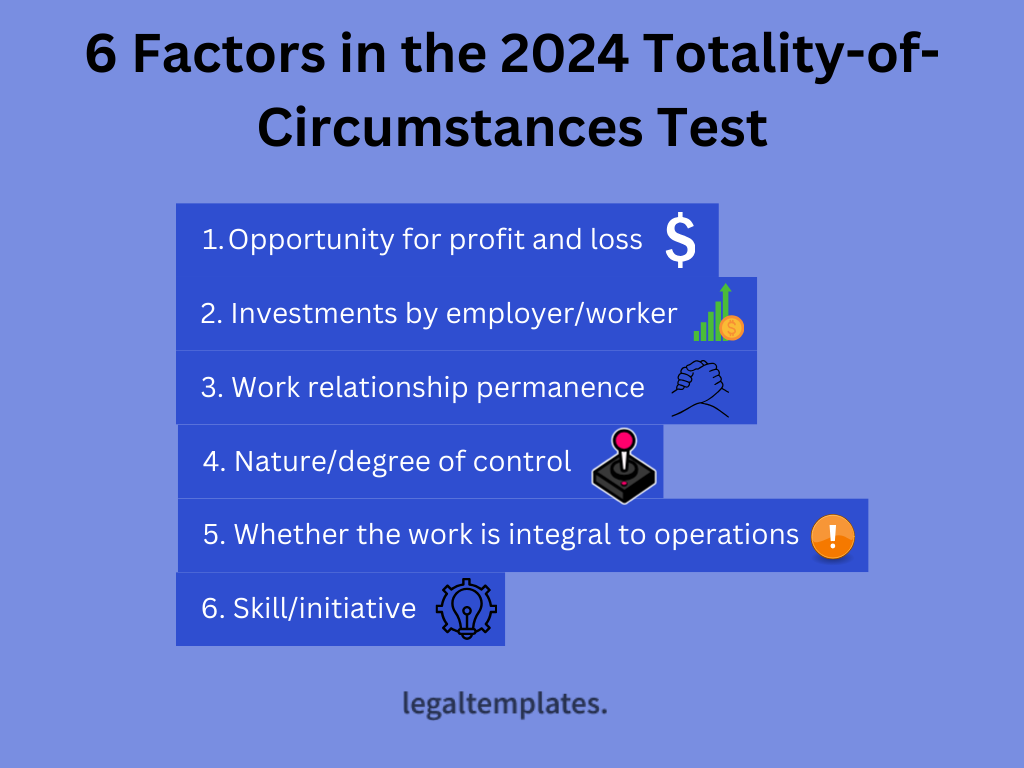

The Department of Labor’s “Totality of Circumstances” Test

The Department of Labor’s “Totality of Circumstances” test evaluates the overall relationship between a worker and employer to determine whether someone is classified as an employee or an independent contractor. No single factor is prioritized, ensuring a balanced approach.

How It Works

The test considers:

- the level of control the employer has over how, when, and where the work is done

- whether the worker can influence their earnings through time management or cost control

- whether the work requires specialized skills and independence

- whether the work is central to the business’s core operations or a supplemental service

By examining all these factors together, the test provides a more accurate assessment of worker status.

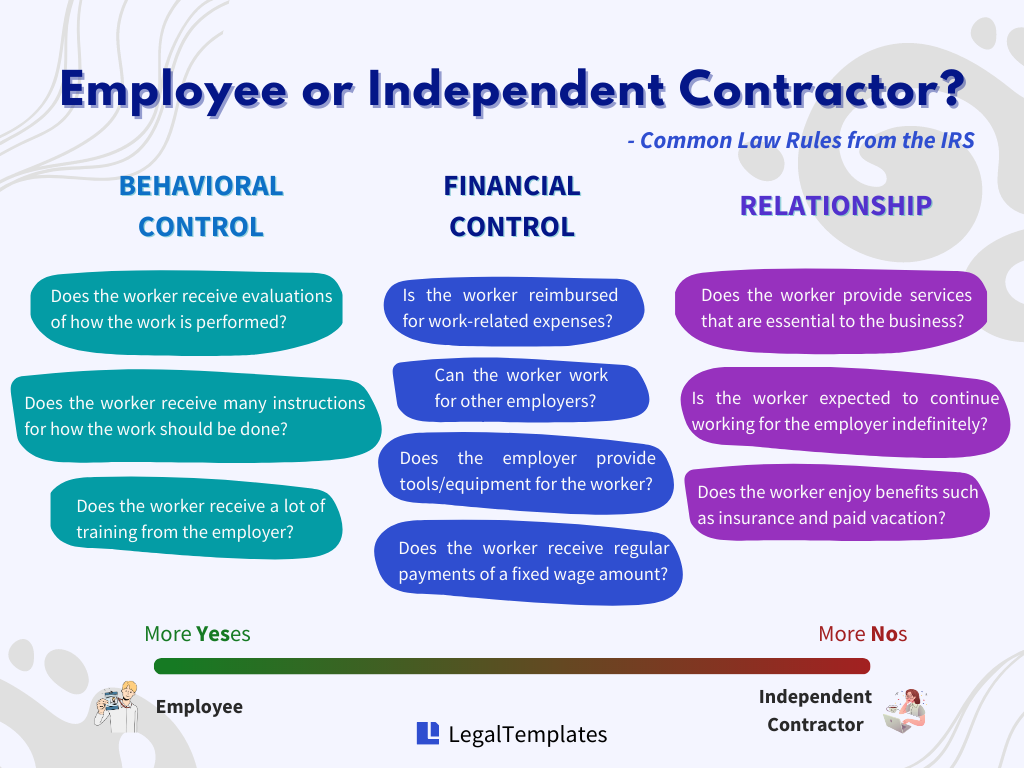

The IRS’s Three-Category Test

The IRS uses three simplified categories to help businesses classify workers correctly:

1. Behavioral Control

This factor examines how much control the company has over the worker’s tasks, training, and supervision.

-

Employees:

- Follow employer-provided schedules, instructions, and training.

- Perform tasks under direct supervision.

-

Independent Contractors:

- Manage their own schedules and work processes.

- Use their expertise to deliver results independently.

If you dictate how, when, and where a worker completes tasks, they’re likely an employee.

2. Financial Control

Here, the IRS considers how the worker is paid and who manages work-related expenses.

-

Employees:

- Receive regular wages or salaries.

- Have expenses covered or reimbursed.

-

Independent Contractors:

- Set their own rates and handle all expenses, like tools, supplies, or overhead.

3. Type of Relationship

The nature of the working relationship often reveals the worker’s classification.

-

Employees:

- Work indefinitely as part of core business operations.

- Receive benefits like health insurance, PTO, and retirement plans.

-

Independent Contractors:

- Perform specific, temporary tasks that are separate from key operations.

- Provide their own benefits and insurance.

Practical Steps for Employers to Classify Workers Correctly

Classifying workers doesn’t have to be complicated. By taking a few proactive steps, you can confidently determine whether to classify a worker as an employee or independent contractor—and avoid costly mistakes down the road.

1. Assess the Role and Scope of Work

Start by clearly defining the worker’s role:

- Is the role short-term or project-based?

- Will you control how, when, and where the work is completed?

- Is the work core to your business operations or more specialized?

If you’re answering “yes” to control or “core business,” the worker may need to be classified as an employee.

Document the role’s requirements and responsibilities—this helps clarify classification and protects your business.

2. Apply the IRS and DOL Tests

Evaluate the worker’s status using these key guidelines:

- IRS Three-Category Test: Behavioral control, financial control, and relationship.

- DOL Totality of Circumstances Test: Consider control, profit/loss opportunity, and the worker’s independence.

Take the time to review all the factors together. If you’re unsure, consult the official IRS and DOL resources.

3. Use Written Agreements

Always create a written contract for independent contractors that clearly defines:

- Scope of work: Deliverables and responsibilities.

- Payment terms: Flat fees, hourly rates, or milestones.

- Timeline: Start and end dates for the project.

Use written contracts, such as an employment agreement or independent contractor agreement, that clearly outline the relationship, duration, and responsibilities. Include language in contracts that clarifies the worker is not an employee and will manage their own taxes and expenses.

4. Review Classification Regularly

Worker roles can evolve over time. Periodically review classifications to ensure they remain accurate:

- Has the worker’s level of control or supervision increased?

- Are they performing more core business functions?

Adjust their classification if necessary to stay compliant.

5. Seek Professional Advice

When in doubt, consult a qualified legal or tax professional. They can help assess worker relationships and ensure your business stays compliant with IRS and Department of Labor rules.

IMPORTANT

File Form SS-8 with the IRS to clarify a worker’s tax status if you’re unsure about their classification.

Tax Obligations for Employees and Independent Contractors

Understanding tax responsibilities is essential for both employers and independent workers. Whether you’re managing a team or working for yourself, knowing what forms to file and what taxes apply will help you stay compliant and avoid unnecessary stress.

Taxes for Employees

For employees, tax management is straightforward because employers handle the heavy lifting.

Employers are responsible for withholding:

- Income taxes

- Social Security taxes

- Medicare taxes

At the end of the year, employees receive Form W-2, which summarizes:

- Total earnings

- Taxes withheld throughout the year

Employers must also report these wages and withholdings to the IRS and the Social Security Administration. This is typically done on a regular basis using forms like Form 941 for quarterly reporting.

Timely wage and tax reporting ensures compliance and prevents costly penalties.

Taxes for Independent Contractors

Independent contractors manage their own taxes, which requires a bit more planning and organization.

Unlike employees, contractors don’t have taxes withheld from their payments. Instead, they’re responsible for paying:

- Income taxes based on earnings

- Self-employment taxes, which include Social Security and Medicare

Clients who pay a contractor $600 or more in a year must provide a Form 1099-NEC. However, if the contractor operates as a C- or S-corporation, this form may not be required.

Businesses that hire contractors must file a 1099-NEC to report these payments to the IRS.

How Legal Templates Can Help

Classifying workers correctly and staying compliant with tax regulations doesn’t have to be complicated. Legal Templates provides easy-to-use tools to streamline the process.

With our Independent Contractor Agreement template, you can quickly create clear, professional contracts that define project scope, payment terms, and timelines. This ensures both you and your contractors are on the same page, protecting your business and simplifying work relationships.

We also make it easy to manage essential tax forms. Use our PDF editor to fill out forms like Form W-2 for employees or Form 1099-NEC for independent contractors. Once completed, forms can be downloaded, printed, and distributed as needed.

Legal Templates helps you save time and reduce stress by providing reliable solutions for worker classification and tax compliance, so you can focus on growing your business with confidence.

Frequently Asked Questions

What rights do independent contractors have compared to employees?

Independent contractors typically do not have access to employee benefits like health insurance, paid leave, or unemployment protections. They operate under contract terms, which define their rights and responsibilities.

How does tax filing differ for independent contractors and employees?

Employees have taxes withheld by their employers and receive a W-2 form. Independent contractors manage their own taxes and receive a 1099-NEC form for earnings over $600.

Can independent contractors receive training from employers?

No, independent contractors are hired for their existing expertise. Providing extensive training could reclassify them as employees.

What are the risks of misclassifying a worker?

Misclassifying a worker can lead to penalties, back taxes, and unpaid wages. It’s important to evaluate worker status based on IRS and Department of Labor guidelines.

What does it mean when a worker Is ‘self-employed’?

Self-employed individuals, such as freelancers or independent contractors, run their own businesses and are responsible for managing their work, clients, and taxes.