All the hard work you’ve put into building your estate should go toward a definitive end. When you make a plan for your estate when you pass away, you can ensure it gets put to use exactly how you wish. Your loved ones will be able to enjoy it, and it won’t be left up to your state’s succession laws. Use our comprehensive estate planning checklist to take charge of your preparation and put your family on the right path.

What Is Estate Planning?

Estate planning involves making arrangements for your properties, money, and investments. Your plan determines what happens to your assets when you pass away. It also enables you to prepare for your incapacitation. This means you can dictate what happens with your stuff if you become unable to act for yourself.

You don’t need millions of dollars or multiple properties for estate planning. Anyone with responsibilities, dependents, or assets can benefit. Estate planning ensures that you keep control over where your hard-earned assets go.

It also helps you provide for your loved ones and reduce legal complications. Protect your wishes and provide peace of mind for your family with a solid estate plan.

A solid estate plan typically includes legal documents like a will, power of attorney, healthcare directive, and trust.

Estate Planning Checklist: How to Create Your Estate Plan

When it comes to setting up an estate plan, you should start by assembling a solid team. Include your family members and loved ones in the conversation. This way, they can step in if there’s confusion about your estate after you pass away or become incapacitated. Ultimately, your plan will be followed, but it helps to have other people in your life who are in the know.

If your estate is particularly large or complex, consider hiring an estate planning attorney. A lawyer can provide specialized knowledge and guidance, giving you more confidence in your preparation. However, Legal Templates offers the forms you need to get started on your own. Our attorney-reviewed documents help you set up instructions for your estate. We walk you through each step, so no legal knowledge is required.

Proceed with the estate planning process thoughtfully, as it can affect your family’s well-being. Follow these 15 steps for estate planning to set yourself up for success.

1. Think About Your Goals

Begin by thinking about what you want to accomplish with your estate plan. If you have children, your primary goal may be to help them fund their education or provide financial support after you’re gone. Still, other goals may include:

- Protect a family business

- Leave most of your assets to charity

- Keep your affairs out of probate court

- Make medical or financial decisions on your behalf

- Handle your debts efficiently so they don’t reduce what your loved ones inherit

- Care for a loved one with special needs without jeopardizing their other benefits

When you know your goals, you can more easily set up your estate plan to meet your needs. These intentions will guide every decision, from choosing documents to naming beneficiaries.

2. Evaluate What You Have

Before you proceed with your estate planning, take inventory of everything you have. This includes tangible and intangible assets, such as the following:

- Cash

- Bank accounts

- Retirement accounts

- Investments

- Life insurance

- Primary home

- Properties

- Vehicles

- Art

- Outdoor equipment

- Collectibles

- Jewelry

This list is not exhaustive, so be sure to account for all assets, including personal belongings.

Assets aren’t all you should account for. You should also evaluate your debts. Before your loved ones can receive any of your assets, all your debts must be cleared. Examples of debts you may need to account for include the following:

- Mortgages

- Home equity lines of credit

- Alimony or child support arrears

- Credit card debt

- Business loans (if personally guaranteed)

- Personal loans

- Student loans

- Vehicle loans

- IRS debt or back taxes

- Unpaid utility bills

- Medical bills

Once you’ve totaled your assets and debts, you can subtract your debt from the value of your assets. This figure is what remains to go to your beneficiaries.

When you calculate what you have early in the estate planning process, you can get a better idea of what your loved ones will receive. Note that the remaining amount, or the residual estate, can change as you sell assets, pay off debt, or make other financial changes.

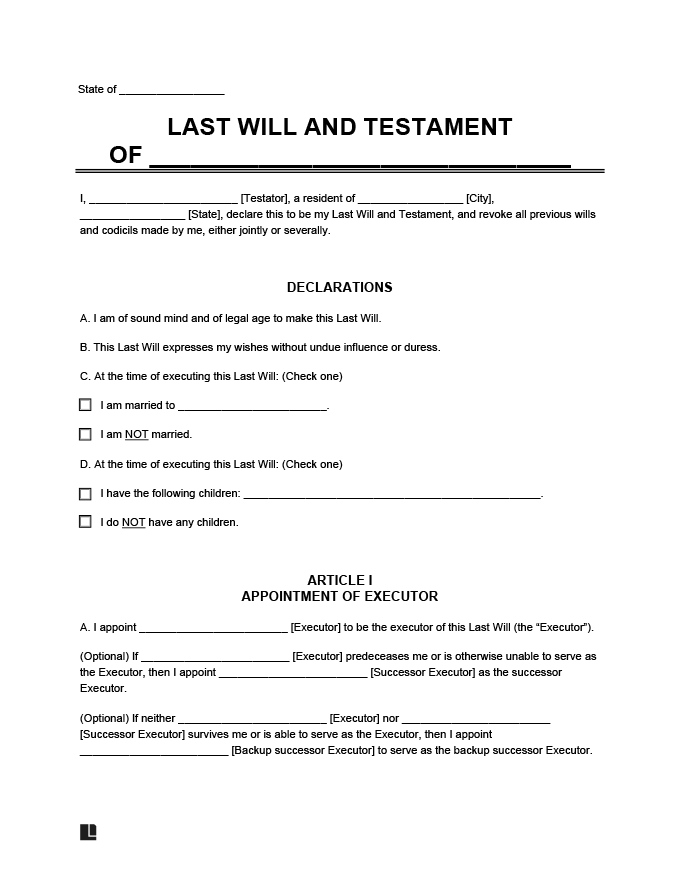

3. Create a Last Will

A last will is a legal document that declares where you want your property to go when you pass away. It can also name guardians for minor children. However, it cannot control assets with named beneficiaries (like life insurance or retirement accounts). If there’s no will, state intestacy laws determine how your assets are distributed. They often won’t align with your wishes, so it’s best to set up your own will while you can.

This document must go through the probate process, meaning a court must validate it and approve the executor named in the will. The executor will carry out the instructions of the will’s author, who is known as the testator. If the court deems the named executor ineligible to serve, it will appoint a new executor.

Need to Update Your Last Will?

Use a codicil to a last will to amend your existing will for minor changes. If the changes you must make are extensive, consider creating a new will.

A last will is only as effective as its clarity, legality, and execution. You must follow your state’s witnessing requirements. Some states require two witnesses, and while notarization isn’t always required, it helps avoid disputes. Be sure also to choose a reliable executor to manage your affairs responsibly.

Not all wills are the same. You may need a distinct type of will, depending on your situation. For example, if the testator is in an emergency where they can only make an oral will, they may select a nuncupative will. (Disclaimer: Nuncupative wills are only valid in some states under strict conditions.) A married couple can elect to create a joint will, as they share assets and beneficiaries. Be sure to choose the right type of will for your situation and goals.

Our recent study found that the typical attorney cost of a last will and testament in the US is $625.

4. Consider a Trust

When reviewing the difference between a will and a trust, the main difference is probate involvement. A will must go through probate when you pass away. If you want a more straightforward way to pass on your assets, consider setting up a trust. As the grantor, you can place certain estate assets into the trust.

When you pass away, the trust manager, known as the trustee, distributes the assets to your named beneficiaries. Because the trust legally owns the assets, the trustee won’t need to get court involvement via probate. Your loved ones can save time and money by skipping probate court. Plus, they can enjoy more privacy, as probate is a public process.

When creating a trust, you must decide if you want it to be revocable or irrevocable. A revocable trust can be changed throughout your lifetime via a trust amendment form, while an irrevocable trust cannot. A revocable trust allows more flexibility as circumstances change, but an irrevocable trust lets you protect assets from creditors and reduce estate taxes.

Other Types of Trusts

While revocable and irrevocable trusts are the two main types, they aren’t the only ones to consider. For example, a testamentary trust is one you can create within your will to lower estate taxes.

You can also create different trusts to meet unique needs. For example, a spendthrift trust helps grantors ensure that beneficiaries aren’t financially irresponsible. Learn more about the different types of trusts to decide which is right for your situation.

5. Appoint a Power of Attorney

If you develop an incapacity and can’t manage your legal or financial affairs, no one will have immediate control over your matters. A family member will have to go through the local court and get appointed as your guardian.

Save them this headache by writing a durable power of attorney. This document lets you name a trusted agent to handle your affairs if you can’t act for yourself. You can grant and withhold certain powers depending on your preferences. Some of these powers include the following:

- Manage funds in checking and savings accounts

- Handle overdue and recurring bills

- Initiate legal claims

- Settle lawsuits

- Transfer assets

- Make gifts

- Buy properties

- Sign contracts

- Update insurance policies

When setting up your estate plan, it’s essential to make your power of attorney durable. If it’s non-durable, it will expire when you become incapacitated. In this case, your agent won’t be able to act for you, rendering the document useless if you cannot make decisions for yourself.

6. Write Your Healthcare Directive

As you age, it’s essential to plan for a decline in your health. While it can vary from state to state, most states recognize an advance directive as a healthcare planning tool. This instrument, also known as a healthcare directive, typically contains two documents: a living will and a medical power of attorney.

A living will lets you outline your treatment preferences for end-of-life care. While you’re mentally sound, you can specify whether you want specific treatments and the extent to which you want them. Here are some of the procedures you can highlight in a living will:

- Surgeries

- Dialysis

- Mechanical ventilation

- Tube feeding

- Resuscitation

- Organ donation

- Life support

Your living will only goes into effect when you become unable to communicate your wishes. It’s a good idea to create it while you’re competent so that medical professionals know what treatments to administer when you’re in an end-stage condition or a vegetative state.

Pair your living will with a medical power of attorney (POA), which lets you choose someone to make healthcare decisions if you’re unable to speak for yourself. While your living will covers specific scenarios, a medical power of attorney ensures that someone you trust can intervene when unexpected situations arise. They’ll have the authority (and your guidance) to make informed choices in your best interest.

Having both a living will and a medical POA helps you ensure your healthcare wishes are followed. When creating both, ensure to adhere to the signing and notarization requirements for your state.

Create a DNR If Desired

As you write your advance directive, consider also creating a DNR order if it fits your preferences. A DNR (do-not-resuscitate) order instructs healthcare providers not to perform CPR if you stop breathing or your heart stops beating. It’s a very specific instruction, but it prevents unwanted life-saving measures for a more natural end-of-life experience.

7. Document an End-of-Life Plan

An end-of-life plan falls outside the scope of property division and legal affairs—it encompasses your final wishes. Use it to explain your funeral plans, such as where you want the funeral to be held, how your remains should be handled, and what funds you want to use to pay for the funeral.

You can also specify whether you want to be an organ donor and to what degree. Some people opt to donate all usable organs when they die, while others only donate certain organs or tissues or elect only to have them used for research purposes. In addition to documenting your preferences in your living will, you can sign up to be an organ donor for guaranteed recognition.

Furthermore, your end-of-life plan can specify your preferred care. For example, you may elect to go to a long-term care facility or have family members move in with you.

Should I Include Funeral Details in My Last Will?

Do not include funeral details in your last will. Since a court must go through probate, it typically won’t be reviewed until after the funeral has already occurred, and your wishes may be seen too late. Instead, outline your funeral preferences in a separate end-of-life document that your loved ones can access immediately.

8. Provide for Minor Children

Family estate planning involves ensuring that your children have financial and custodial care when you’re gone or unable to care for them. Use your last will to appoint a trusted adult as the legal guardian to take over physical custody of your children if you pass away or can no longer fulfill your role as their parent or guardian.

You can also designate someone to manage your children’s inheritance until they come of age. This person can be the same as your guardian, but it can also be someone different. You may also set up a trust to manage the funds you leave behind, ensuring the trustee distributes the money according to your instructions, such as for your children’s living expenses or education.

Depending on your circumstances, you may need to set up more temporary plans to ensure no disruptions occur with your children’s care. For example, if you are recovering from surgery, you can write a minor power of attorney to grant temporary caregiving authority. Some states have limitations on the powers granted in this form, so be sure to check your area’s guidelines.

Another temporary tool for children’s well-being is a child medical consent form. This form lets someone make medical decisions for your child if you’re unavailable. It’s useful when children travel or stay with relatives, as you can ensure they have someone to consent to surgeries or other medical treatment as needed.

Is Your Child Traveling?

If your child is traveling, use a child travel consent form to authorize their solo trip or travel with an adult who is not their parent or legal guardian.

9. Determine Business Ownership

If you own a business, your estate plan should include what happens to your share of the business when you pass away. The outcome largely depends on your business structure:

- Sole proprietorship: The business will dissolve upon your death, as there is no legal separation between you and the business.

- LLCs, corporations, and partnerships: These structures may continue operating, but it depends on what’s outlined in the governing documents. Your LLC operating agreement, corporate bylaws, or partnership agreement will dictate what happens.

To ensure a smooth transition, consider the following as part of your estate planning checklist:

- Buy-sell agreement: A buy-sell agreement outlines how ownership interests will be transferred after a death, disability, or retirement. It can help prevent disputes and ensure a fair valuation.

- Ownership transfer plans: Clarify whether heirs will take over or if your shares should be sold to co-owners or a third party.

- Valuation and tax planning: Business succession may have tax implications. Plan in advance to minimize surprises and ensure continuity.

Be sure to set up a solid plan to ensure your business doesn’t face unnecessary disruption, legal challenges, or dissolution.

10. Account for Digital Assets

When it comes to estate planning suggestions, you may not think about your digital presence. However, it’s essential to account for your digital assets. Access to file storage services, social media accounts, bank accounts, and mobile payment services can be difficult for your family members to recover if you don’t plan in advance.

Create a list of all relevant accounts and login information. Do not include this information in your will, as it will become part of the public record. Instead, use an online password manager or place a written copy in a lock box. Ensure that a trusted individual has instructions on accessing your login details when you pass away or become incapacitated. With a plan in place, you can prevent unclaimed funds and lost sentimental items like photos and videos.

11. Obtain Life Insurance

If you don’t already have a life insurance plan, consider getting one to provide your loved ones with immediate financial support after your death. Unlike many estate assets that may take time to go through probate, life insurance benefits are typically paid out quickly and directly to your named beneficiaries. This can help:

- Cover funeral and burial costs

- Pay off outstanding debts or a mortgage

- Replace lost income for dependents

- Fund a child’s education

- Provide long-term financial stability

You may have life insurance through your employer’s benefits package. If the amount is low or you want additional security, you can purchase supplemental life insurance through an insurance provider. Including life insurance in your estate plan ensures your family isn’t left financially vulnerable during a difficult time.

12. Name Beneficiaries for Certain Accounts

Certain financial accounts are designed to pass directly to a beneficiary upon the account holder’s death. These include:

- 401(k)s and other employer-sponsored retirement plans

- Individual Retirement Accounts (IRAs)

- Life insurance policies

- Payable-on-death (POD) bank accounts

- Transfer-on-death (TOD) investment accounts

- Annuities

- Health savings accounts (HSAs)

These accounts need a designated beneficiary because they are non-probate assets. This means they bypass your will and go directly to the named beneficiary, speeding up access to funds and avoiding probate court entirely.

Don’t let your accounts sit without a beneficiary. Update the beneficiary designations for all relevant accounts and review them regularly to ensure the designations reflect who you want the funds to go to.

13. Plan for Estate Taxes

One of the most important estate planning tips is to plan for potential estate taxes that could affect your loved ones. Without proper preparation, estate taxes can significantly reduce the value of what your beneficiaries receive. To reduce or eliminate estate tax liability, consider the following strategies:

- Use the estate tax exemption: Each individual can pass on a certain amount tax-free (known as the IRS lifetime exemption).

- Make lifetime gifts: Giving assets while you’re alive can reduce the size of your taxable estate. You may need to use a gift affidavit to confirm that the transaction is a gift.

- Use portability between spouses: Unused exemption amounts from one spouse can be transferred to the other to maximize tax savings.

- Create a generation-skipping trust: This allows assets to pass tax-efficiently to grandchildren or later generations.

- Use estate freezing techniques: Transfer future appreciation of assets to beneficiaries now to lock in today’s value for tax purposes.

Prepare for Possible Income in Respect of a Decedent (IRD) Taxes

Another tax you should be aware of when estate planning is the income in respect of a decedent (IRD) tax. This tax applies if you were entitled to income but didn’t receive it before you passed away. Examples of income subject to IRD tax include rental income, unpaid wages, and uncollected retirement account distributions.

The recipient of IRD must report it on their tax return so they can pay the appropriate IRD tax. Note that while the IRD tax is not technically the estate tax, it’s a tax issue that arises due to someone’s death. It’s important to plan for IRD so that beneficiaries aren’t surprised by a tax bill for the income they inherit.

14. Store Your Plan in a Safe Place

Once you create your plan, store it in a safe place. This may be in a fireproof home safe, a safety deposit box, or a locked filing cabinet. Ensure a trusted person knows the location and has access if you pass away or become incapacitated.

Also, record POAs with financial institutions, like banks or credit unions, so they know the powers entrusted to your elected agents. You should also record medical POAs with the facilities where you receive care. This will make it easier for doctors and other professionals to know who has the authority to decide or withhold your treatment.

15. Revisit as Needed

Once you create your estate plan, you shouldn’t forget about it entirely. Instead, keep it in the back of your mind and know when to update it. Ideally, you should revisit your estate planning checklist to account for significant life events, such as:

- Having a child

- Getting divorced

- Developing a sickness or disability

- Relocating to another state

- Selling or buying property

- Starting a business

- Receiving an inheritance

If you experience a change in your relationship with an agent or executor and no longer trust them, you should also update your estate plan. Even if you don’t experience these big changes, you should revisit your plan every three to five years. Reviewing your plan regularly can help ensure it still aligns with your wishes.