When you’re gone, you want to ensure your loved ones are cared for, not tied up in legal red tape. That’s why understanding probate is essential. If you don’t plan ahead, some of your assets could get stuck in a lengthy and costly legal process, making it difficult for your family to access their inheritance. Let’s explore what probate involves and, more importantly, how you can help your loved ones avoid it.

What Is Probate?

Probate is the legal process of handling a person’s affairs and assets after their passing. In probate, the courts authenticate the will, officially appoint an executor, and distribute assets. This process allows beneficiaries or creditors to claim their share of the estate.

Each state has its own laws that dictate what kinds of estates need to go through probate. Other factors, such as the size of the estate and the debts and assets involved, also affect probate. The exact probate process may also differ depending on whether the deceased had a valid will.

Legal Templates offers estate planning forms and resources to help make probate quick and painless. Protect your loved ones and estate with our legally-compliant last will and testament template.

What Goes Through Probate?

While not every asset or estate has to go through probate, certain factors make it necessary for the court to review and distribute them accordingly. Depending on ownership status and protections, each part of your estate may qualify as a probate or non-probate asset. Use the following information to determine which assets may go through probate.

Probate Assets

Each state has its own probate laws and processes, but many include similar guidelines for the types of assets that must go through probate. Typically, the courts must validate and distribute assets held solely by the deceased. The most common types of assets that require probate include:

- solely owned real estate

- financial accounts without a payable-on-death clause

- vehicles

- personal property

- business interests

Non-Probate Assets

When assets are shared or explicitly assigned to beneficiaries, it may mean that probate is not necessary. The requirements for these assets can also depend on state and local laws. The following property and estates may qualify as non-probate assets:

- beneficiary assets

- living trusts

- transfer-on-death trusts

- survivorship rights

- small estates (beneath the state maximum)

- life insurance policies

- retirement accounts

The Probate Process

When a person dies and leaves behind their estate, the courts may step in to begin the probate process. This process validates and distributes assets using the following steps:

- Appointing an executor: The court approves the executor named in the will to oversee the probate process and handle the division of the estate. If the court believes the named executor cannot complete their duties, it will appoint a new executor. Sometimes, the deceased names an alternate executor for this purpose. If there’s no valid will, the court may nominate an administrator or executor, typically a family member or spouse of the deceased.

- Validating claims and documents: The court reviews the legal validity of the individual’s death certificate, will, and claims from creditors. They will also review the inventory of assets within the estate. Gathering the necessary documentation ensures each part of the estate is legally owned and correctly divided.

- Distributing assets: After reviewing the documents, inventory, and claims, the executor distributes the assets according to the terms of the will, intestacy laws, or local regulations. Any debts or costs are taken out of the estate first, and the remaining assets are divided among the designated beneficiaries or next of kin.

- Handling disputes: Disputes over the estate and debts can arise during probate. The court or executor settles heirship, valuation, and title disputes to complete the distribution.

- Reporting and approving: After settling the estate, the executor provides the court with a report listing each heir and asset. The court reviews the report to ensure proper handling before closing the estate and ending the probate process.

How Much Does Probate Cost?

The probate process and the required documents or legal help can become costly. The American Association of Retired Persons (AARP) estimates that probate costs can average about $1,500. Generally, the costs associated with undergoing probate are covered by the estate. The total expenses are deducted from the total value of the assets. Consider the following factors that can affect how much probate costs:

- Court filing fees: Starting the probate process requires you to file the estate documents and death certificate with the court for a fee. This fee typically ranges from $45 for small estates to $1250 for high-value estates.

- Legal consultation fees: If you hire or consult a legal professional for help with probate, expect to pay an hourly or consultation fee. Exact costs depend on the scope of their work and factors such as experience and location, and typically range from a few hundred dollars to over a thousand. If you end up hiring an attorney, expect to pay a retainer fee and their hourly rate.

- Executor fees: The estate executor may incur expenses for travel, time, and administrative work related to distributing assets. Generally, the estate provides the funds necessary to cover the executor’s required spending.

How Long Does Probate Take?

The probate process’s steps, complications, and outcomes vary for each case, affecting the probate period’s length. According to the American Bar Association, the average time for a probate case is between six and nine months. The most common factors that impact the duration of a probate case include:

- estate size

- type and complexity of assets

- amount of claims submitted by creditors

- number of beneficiaries

- legal disputes or someone contesting the will

- state and federal tax processes

- state laws or documentation requirements

What Are the Tax Implications of Probate?

When you pass away, your estate and probate assets become subject to different types of taxes. Some of these can be avoided or minimized with effective estate planning, but it’s common for beneficiaries to face tax charges. The most common taxes include:

- Capital gains tax: If a beneficiary sells an inherited asset, they must pay a capital gains tax on any profit made from the sale. The tax is a set percentage of the profit, which can vary depending on the seller’s income bracket and how long they have held the asset. The taxable gain is calculated using the sale price minus the item’s fair market value when the beneficiary received it.

- Federal estate taxes: At the time of death, the fair market value of your assets is totaled and used to determine the amount owed for federal estate taxes. The assets needed to cover tax payments are deducted from your distributable estate.

- Inheritance taxes: Pennsylvania, New Jersey, Kentucky, Iowa, Maryland, and Nebraska charge beneficiaries with an inheritance tax, separate from federal estate taxes. These tax charges depend on the size of your inheritance and state guidelines.

How to Avoid Probate

You can avoid probate for some assets with proper estate planning. Establishing arrangements with their own transfer mechanisms allows you to transfer property to your desired heir without the hassle of probate. Consider the following five best ways to avoid probate.

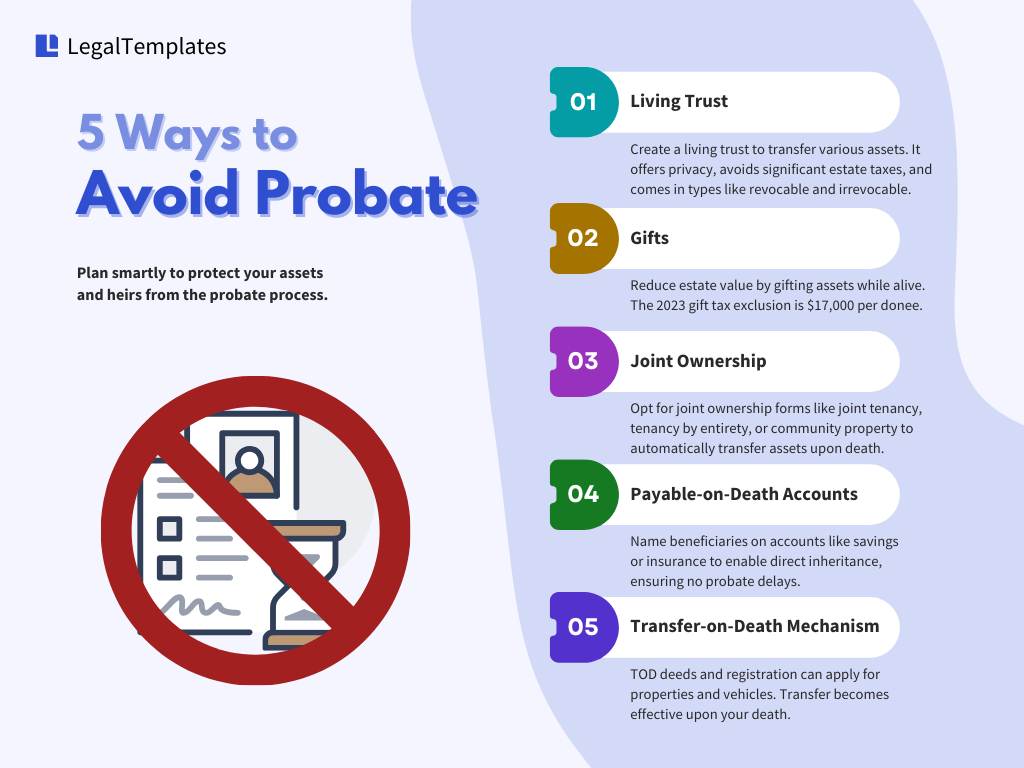

1. Create a Living Trust

Placing assets into a living trust helps to avoid probate by ensuring a direct transfer of ownership after your passing. Establish a living trust and add your desired bank accounts, real estate, vehicles, or personal property. Appoint a trustee to oversee the trust and name the beneficiaries for easy distribution.

A living trust also provides other benefits, such as an added layer of privacy and protection against estate taxes. The contents and distribution of a trust remain private. You can also use the different types of trusts depending on the assets you want to protect and your desired terms.

2. Gift Assets

Passing along assets as a gift provides an easy way to transfer ownership and avoid probate. If you transfer assets while alive, they no longer count as part of your estate and can bypass probate and taxes. Gifting your property provides immediate benefits for your heirs, but requires you to give up control and ownership of assets.

For the 2025 tax year, the IRS sets the annual gifting limit as $19,000 per donee. This means you can gift each person assets up to $19,000 in value without paying gift tax on the transfer, and there is no limit to the number of recipients per year. Ensure you check regulations for the lifetime gifting limit for the total value of gifts you can provide without facing extra taxes.

3. Establish Joint Ownership

You can add your loved ones as co-owners for any property with a title. Designating them as co-owners provides a way to transfer ownership without the probate process. Co-ownership may take many forms depending on your property, needs, and local laws. The types of joint ownership include:

- Joint tenancy with right of survivorship: In a joint tenancy situation, two or more individuals own the property together. This allows for the automatic transfer of ownership if one of the individuals passes away.

- Tenancy by the entirety: About half of the states recognize tenancy by the entirety for married couples. This identifies the couple as a single legal entity and gives each individual total ownership, meaning the surviving spouse keeps ownership without probate.

- Life estate: An individual may choose to transfer property to a beneficiary during their lifetime but retain a life estate, allowing them to continue living on the property until their death.

- Community property: Certain states, such as Arizona, California, and Texas, operate under community property laws, stating that property acquired during a marriage is owned equally by each party. In this case, the spouse maintains property ownership without probate proceedings.

4. Designate Payable-On-Death Accounts

Payable-on-death (POD) accounts let you assign your financial assets to beneficiaries. A POD account allows for the inheritance of funds without a letter of testamentary or probate proceedings. You maintain ownership of these funds during your lifetime, and they pass to your named heirs after your death. This type of account can be beneficial for life insurance policies, pension funds, retirement accounts, regular checking and savings accounts, money market accounts, and 401(k) earnings.

If your executor is also the beneficiary of your account, a POD offers additional ease and benefits. Unlike a regular bank account, a POD will not freeze the account or require the executor to present a death certificate or letter of testamentary.

5. Make Transfer-On-Death Deeds

Transfer-on-death (TOD) deeds make passing real estate or vehicle ownership to your beneficiaries easier. This type of deed allows you to keep control and ownership of your property during your lifetime and only transfers after your death. For vehicle transfers with a TOD deed, the named beneficiary just needs to provide the vehicle’s title and the death certificate.

The Uniform Transfer on Death Securities Registration Act also permits you to designate beneficiaries for stocks, bonds, and brokerage accounts. Like TOD deeds for properties, you keep control over the assets, allowing you to manage or sell them.

Probate Laws by State

As mentioned, each state may have different probate processes and laws. These laws include information about the period for executors to file a will and guidelines for property division. The table below shows each state’s specific probate laws.

| State | Probate Laws |

|---|---|

| Alabama | AL Title 43, Chapter 8 |

| Alaska | AS Title 13, Chapter 16 |

| Arizona | AZ Title 14, Chapter 3 |

| Arkansas | AK Title 28 |

| California | CA Probate Code |