If you’re lending or borrowing money, it’s essential to select the correct type of promissory note to reflect the terms of the agreement. Your promissory note should detail the type of loan and the terms of the repayment schedule.

A promissory note is a legally binding written promise that a borrower will repay a lender a determined sum of money and interest. The frequency, amount, and payment schedule depend on the promissory note and the agreed-upon repayment option.

Types of Promissory Notes

Select the type of promissory note that best represents why both parties agreed to the loan.

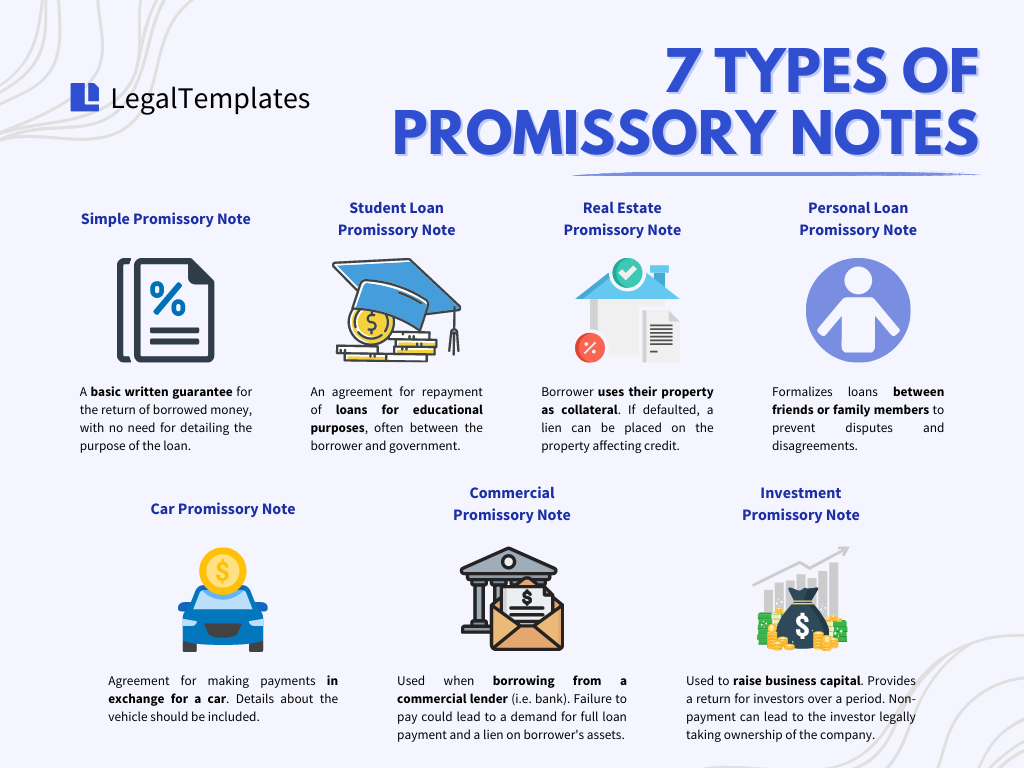

Simple Promissory Note

A simple promissory note creates a written guarantee that the borrower will repay the loan to the lender in an agreed-upon manner. Unlike the secured promissory notes described below, the purpose of this type of promissory note is relatively straightforward and requires no collateral.

Student Loan Promissory Note

A student loan promissory note is a master promissory note created by the government to ensure that borrowers will repay their loans for education, including the interest charged.

Although student loan promissory notes are primarily between a borrower and the government, some students create them with their parents or relatives who pay for their education.

Real Estate Promissory Note

A real estate promissory note is when a borrower uses their property as collateral to secure the loan. If a borrower defaults, the lender can place a lien on the property; such information can become a public record and affect the borrower’s credit.

Personal Loan Promissory Notes

A personal loan promissory note documents a loan between friends or family members. It can be tempting to forego formal documents when lending money to loved ones. However, regardless of how well you know someone, having a written record of the loan can help prevent unforeseen disagreements.

Car Promissory Note

A car (vehicle) promissory note creates an agreement that a borrower will make payments to a lender in exchange for a car. The note should include details about the make and model of the vehicle and be kept somewhere accessible in case ownership of the car needs to be proven.

Suppose you want to transfer property, such as a car, without asking for payment. In that case, a gift affidavit allows you to record the change of possession legally.

Commercial Promissory note

Commercial promissory notes are used when borrowing money from a commercial lender like a bank or loan agency. If the borrower cannot make the required payments, the lender may demand full loan payment – including interest. Furthermore, the lender can assign a lien on assets the borrower owns until payment is received.

Investment Promissory Note

An investment promissory note, often a substitute for a business loan, is used to raise business capital. Investment notes reduce the risk of investing in a company by ensuring investors receive a return over time. If the borrower fails to pay the money, the investor can legally take ownership of the company.

Types of Repayment Options

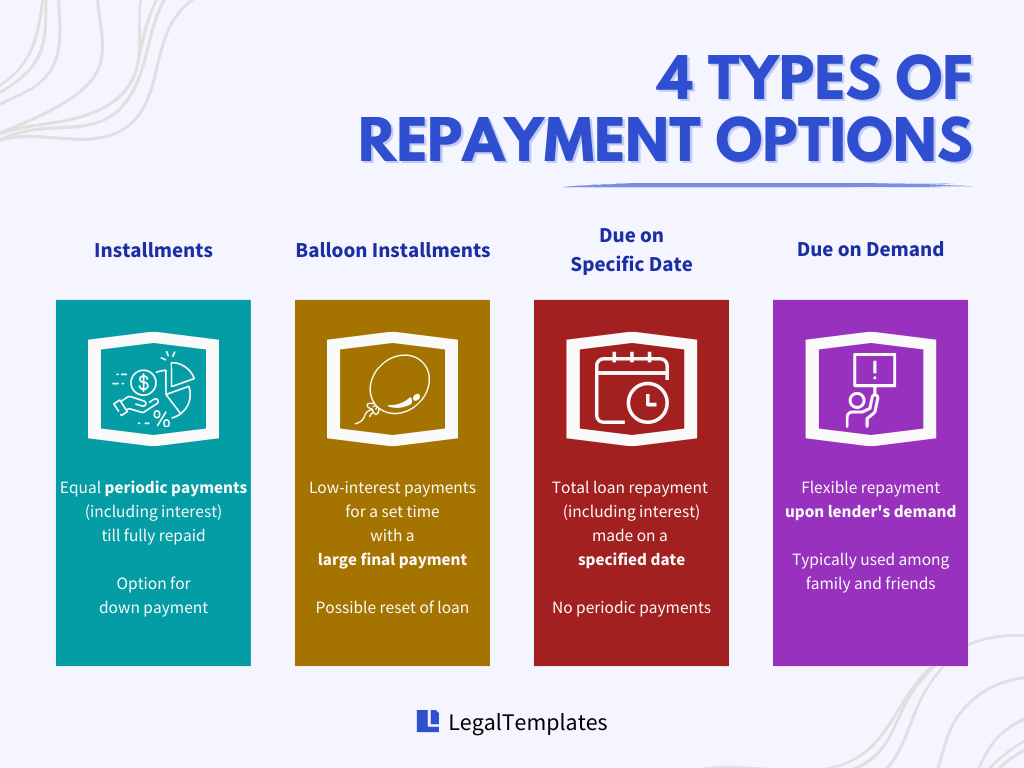

Typically, there are four ways for a borrower to repay money and interest to a lender.

Installment Payments

Installment payments are expected for expensive purchases like cars, boats, and appliances. Usually, the payments are made in equal monthly amounts, including interest, until the principal balance (the total amount borrowed) is completely repaid.

Borrowers can afford to make a down payment on an installment loan to reduce the total amount of interest paid.

Installment Payments with a Final Balloon Payment

Balloon payments are frequently used in mortgage loans and are typically used by short-term borrowers because they feature lower interest rates than long-term loans.

In a balloon payment, the borrower agrees to pay a low interest rate for some time, such as five years, and pays back only a fraction of the principal balance.

At the end of the term, the borrower can reset the loan (potentially at a higher interest rate) or pay off the massive remaining balance (the balloon) if they can afford it.

Due on a Specific Date

Borrowers and lenders can agree to a specific payback date for smaller loan amounts. Lenders will know when the loan will be paid back, and borrowers will not have to worry about monthly payments. Instead, the borrower repays the entire amount of the loan—the principal plus any interest—on a specific date.

Due on Demand

Due-on-demand notes are typically for loans between family and friends. As there are no specific payment terms, these loans are sometimes called open-ended loans.

Borrowers can pay back the note when they’re financially stable, and lenders can ensure they’ll have an income source if necessary. If a note does not have payment terms, it’ll be considered due on a demand note.

Whichever repayment option you and other involved parties opt for, detail it on your note and abide by it strictly. Failing to outline payment amounts and schedules can confuse, cause unmet expectations, strained relationships, and even take legal action.