What Is a Credit Dispute Letter?

A credit dispute letter lets you contest inaccurate or outdated information on your credit report. Per the Fair Credit Reporting Act (FCRA), you can challenge items that are unfairly reported.

This letter is a key tool in managing your credit history. It names your disputed items and the reasons for the disputes, with supporting facts. Once it’s written, you can send it to one of the three major credit bureaus.

The recipient will review your request to correct the false details and investigate the issue. If necessary, it will update your credit report to reflect the accurate history.

What Items Can You Dispute?

If you’re wondering what you should do if there are incorrect transactions on your monthly statement, one important step is to dispute them through the credit reporting agencies. But that’s not the only error you can challenge on your credit report. Other items you can dispute include:

- Incorrect account details: Mistakes in your name, address, or Social Security number.

- Payment errors: Payments that you made on time but were incorrectly reported as late.

- Duplicate entries: The same account appears more than once, making it look like you owe more than you do.

- Outdated information: Old debts that should’ve been removed from your report.

- Incorrect credit limits: Credit limits that appear lower than they are, which can affect your credit utilization ratio.

- Questionable accounts: Loans or credit cards opened fraudulently.

Review your credit report regularly to detect any errors. If you find any, take action as soon as possible by informing one of the three major credit bureaus. You can also notify the company that provided the incorrect information (the “furnisher”), as they may need to update their records.

Are You a Victim of Identity Theft?

If you need to dispute an item on your credit report because someone has stolen your identity, you can report identity theft through the Federal Trade Commission. You may need to complete various steps, including filling out an affidavit of identity.

How to Write a Credit Dispute Letter

Your credit report dispute letter should be concise yet thorough to accurately describe the issue. Follow these steps to write an effective letter.

1. Identify the Involved Parties

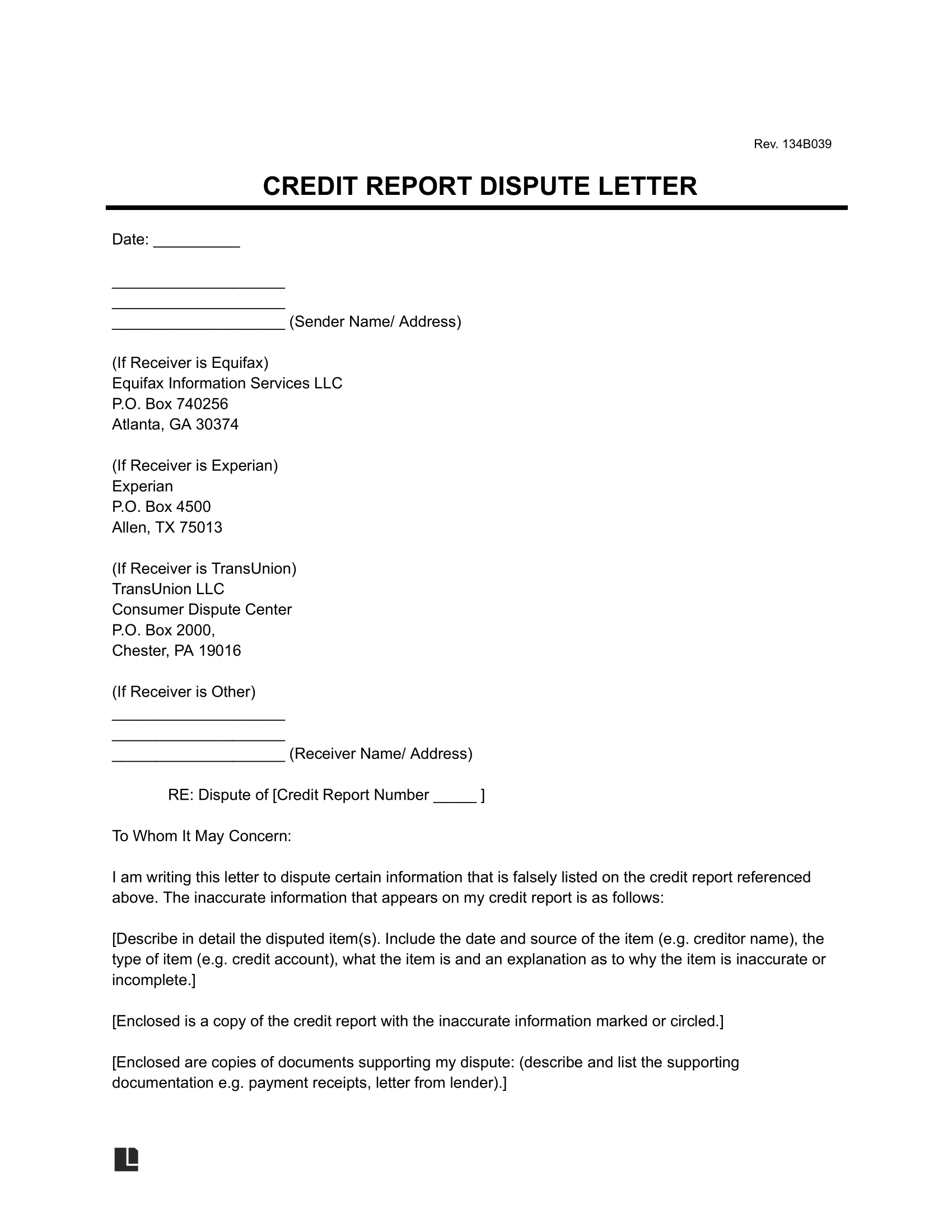

Identify yourself as the sender, as you are the party disputing an item on your credit report. Provide your name, address, and contact details.

Address the receiver, who will likely be one of the three major credit bureaus. When you use Legal Templates’s form, you can choose which one, and we’ll automatically fill in their address for you:

- TransUnion: TransUnion LLC, Consumer Dispute Center, PO Box 2000, Chester, PA, 19016

- Experian: Experian, PO Box 4500, Allen, TX 75013

- Equifax: Equifax Information Services LLC, PO Box 740256, Atlanta, GA 30374

If you send the letter to another credit reporting agency or financial institution, you can fill in their name and address instead.

2. Explain the Information You Want to Dispute

Review a copy of your credit report from one of the three major credit bureaus. Determine any inaccuracies you want corrected.

Include the date and source of the disputed information, and describe why it’s inaccurate. Explain that you want the error corrected or removed from your credit report.

3. Provide Supporting Documentation

Include supporting documentation to help the credit bureau with its investigation. One key piece of evidence is a copy of the original credit report with the disputed items highlighted or circled. This makes it clear what items you’re challenging. You may also provide other supporting documents to show why specific information is wrong:

- Receipts for bills paid on time

- Letters from creditors confirming account closures or balance updates

- Account statements from lenders or creditors

- Bank statements showing correct transactions or payments

- Court documents for bankruptcies or liens that have been satisfied or dismissed

4. Sign Your Name

Sign and print your name to confirm that the information you’re providing is accurate. Your signature also verifies that you’re the person authorized to request changes to your credit report. Some credit bureaus won’t look into a dispute without your signature, so ensure to include it to show you’re making a legitimate request. You should also make sure to follow any other procedures that are required by the credit bureau in order to submit and finalize your dispute.

Dispute Sample Letter to Remove Collection from Credit Report

View our free sample credit dispute letter to understand its format. When you’re ready, create your own using our guided form. Download a final version in PDF or Word format.

How to Send a Dispute Letter to Credit Bureaus

Once you write your credit report dispute letter, mail it to one of the three major credit bureaus listed above: Experian, Equifax, or TransUnion. You may also consider sending your dispute to all of the bureaus in order to ensure the inaccurate information is completely removed. Send it via certified mail with a return receipt to ensure the bureau receives it.

The bureau will have 30 days to complete its investigation. If it needs additional information from you, it can take up to 45 days. Once the bureau finishes its investigation, it must notify you of the results within five days.

Other Ways to Dispute an Inaccurate Credit Report

If the credit bureaus don’t correct the inaccuracies after your dispute, you can take the following actions:

- Request an investigation reconsideration: Provide additional evidence to support your claim.

- File a complaint with the Consumer Financial Protection Bureau (CFPB): The CFPB oversees credit reporting agencies and may help resolve the issue.

- Consult an attorney: Consider seeking legal counsel to explore your options for further action.

You can also contact the debt’s furnisher (like your credit card company). Send them a debt validation letter, asking them to prove they have a legal right to collect the debt.

When Does Negative Information Go Off My Credit Report?

If all else fails, you may wait seven years for negative information to go off your credit report, per the FCRA. Most negative information will be removed from your report after seven years, but you will still be legally obligated to pay it off.