What Is a Debt Validation Letter?

A debt validation letter is a written request sent to a debt collector to ask for proof of a debt. You send it after a collector contacts you to confirm the debt is real, yours, and accurate, before taking any next steps.

Under the Fair Debt Collection Practices Act, collectors must first send a written notice with details about the debt, usually within five days of first contact (12 C.F.R. § 1006.34(a); 15 U.S.C. § 1692g).

Once you receive that notice, you have a chance to review the debt before taking any action. It outlines the amount owed, the creditor, and your right to dispute it. A debt validation letter takes the next step. You can ask for more details, raise concerns, or dispute the debt in writing.

That added step can work in your favor. It slows things down by requiring the collector to back up the claim with documentation before moving forward. This is especially important if you don’t recognize the debt, if the amount seems wrong, or if the account may already be paid or too old to collect.

Debt Validation vs. Debt Verification

Debt validation and debt verification are easy to mix up:

- Debt validation: The collector gives you details so you can confirm the debt is yours and accurate.

- Debt verification: The collector reviews your claim and investigates it after you dispute the debt.

When to Use a Debt Validation Letter

Use a debt validation letter when you need to confirm a debt before taking any action. It helps you pause, review the details, and avoid paying or agreeing to something that may be incorrect. Common situations include:

- After a debt collector contacts you. Send it once you receive a call or written notice about an alleged debt.

- If you don’t recognize the debt. Use a debt validation request letter to check whether the account actually belongs to you.

- If the amount seems wrong. Ask for a breakdown so you can confirm fees, interest, and totals.

- Before paying or agreeing to anything. Don’t commit until you’ve reviewed the details.

- When you want to verify the debt before responding. It gives you time to confirm accuracy and decide your next step.

- If you need documentation first. You’re not expected to respond or pay until you’ve had a chance to review the debt information.

In real life, these situations can overlap. For example, you might get a notice about an account that looks familiar, but the balance feels off. Legal Templates can help you send a clear request quickly, so you can get the details you need before deciding what to do next.

You have a 30-day validation period after receiving the notice. If you miss that window, the debt may be assumed valid.

How to Write a Debt Validation Letter

Keep your debt validation letter direct and specific. You’re asking the collector to prove the debt, so include enough detail for them to identify the account and respond properly. Here’s what to do.

- Add your contact details. Include your full name, mailing address, email, and phone number so they can match your request to the right file.

- List the collector’s information. Use the correct company name and mailing address from their notice.

- Note the contact details. Reference how and when they reached you (mail, phone, email) so there’s a clear record.

- Identify the account. Include the account number and type of debt, if available, to avoid any confusion.

- Request verification clearly. State that you’re asking for proof of the debt before taking any next step.

-

Ask for specific documents and details. Focus on what you need to confirm accuracy:

- Creditor’s name and address

- Full account number

- Amount owed and how it was calculated

- Original delinquency or charge-off date

- Supporting documents or a signed agreement

- State your position. Make it clear that you dispute the debt or need confirmation before paying.

- Sign and date the letter. This creates a clear timeline for your request.

A few clear lines can shape how the collector responds. If your request is vague, you’ll likely get incomplete answers or more follow-ups. A focused debt validation letter helps you get the full details upfront and gives you a stronger record if you need to escalate later.

If the debt looks incorrect, send a credit dispute letter to challenge it. If the collector keeps contacting you without resolving the issue, you can also send a cease and desist letter to stop further communication.

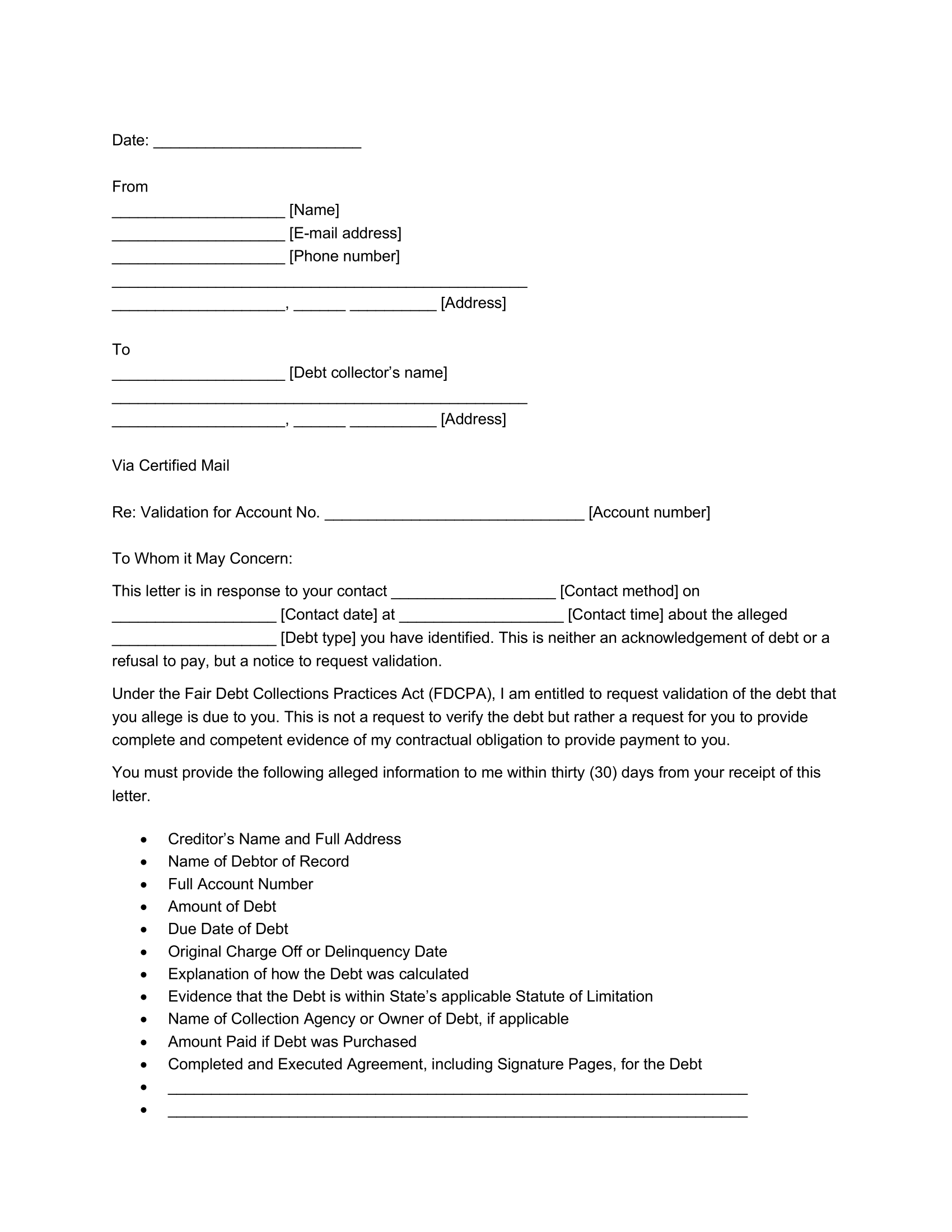

Example of a Debt Validation Letter

Here’s a completed debt validation letter based on a credit card account sent to a collection agency. It shows how to reference the account, request proof, and list the details you want confirmed.

Date: May 1, 2026

From

Jordan Smith

[email protected]

(917) 555-3821

145 West 86th Street, Apt 7C, New York, NY 10024

To

Midland Credit Management, Inc.

350 Camino De La Reina, Suite 100

San Diego, CA 92108

Via Certified Mail

Re: Validation for Account No. 542178963

To Whom it May Concern:

This letter is in response to your contact by mail on April 26, 2026, about the alleged credit card debt you have identified. This is neither an acknowledgment of debt nor a refusal to pay, but a notice to request validation.

Under the Fair Debt Collection Practices Act (FDCPA), I am entitled to request validation of the debt that you allege is due to you. This is not a request to verify the debt but rather a request for you to provide complete and competent evidence of my contractual obligation to provide payment to you.

You must provide the following alleged information to me within thirty (30) days from your receipt of this letter.

- Creditor’s Name and Full Address

- Name of Debtor of Record

- Full Account Number

- Amount of Debt

- Due Date of Debt

- Original Charge Off or Delinquency Date

- Explanation of how the Debt was calculated

- Evidence that the Debt is within the State’s applicable Statute of Limitation

- Name of Collection Agency or Owner of Debt, if applicable

- Amount Paid if Debt was Purchased

- Completed and Executed Agreement, including Signature Pages, for the Debt

Pursuant to my rights under the FDCPA, I will be ignoring any future collection attempts until you verify that this debt is mine.

Thank you for your consideration.

Sincerely,

Jordan Smith

How to Send a Debt Validation Letter

Send your debt validation letter in writing so there’s a clear record of your request. Mail it by certified mail with a return receipt. That gives you proof that the collector received it and when they got it.

Keep a copy of your debt validation letter and your mailing receipt for your records. You may need them later if there’s a dispute or if the issue escalates. After sending the letter, wait for a response before making any payments or agreeing to the debt. This gives you time to review the details and confirm everything is accurate.

Once you send the letter, the collector must pause collection of the disputed debt until they respond. They need to provide verification or more details about the debt. If they can’t verify it, they may not continue collecting.

Can I Send a Debt Validation Letter After 30 Days?

You can send a debt validation letter after 30 days, but you lose the automatic protections offered by the FDCPA. Debt collectors may still respond to reasonable requests made after the 30-day deadline to avoid legal disputes.

Sample Debt Validation Letter

View a completed debt validation letter to see how details like the creditor’s information, account number, amount owed, and validation request are included. Then, customize and download the debt validation letter template in Word and PDF.