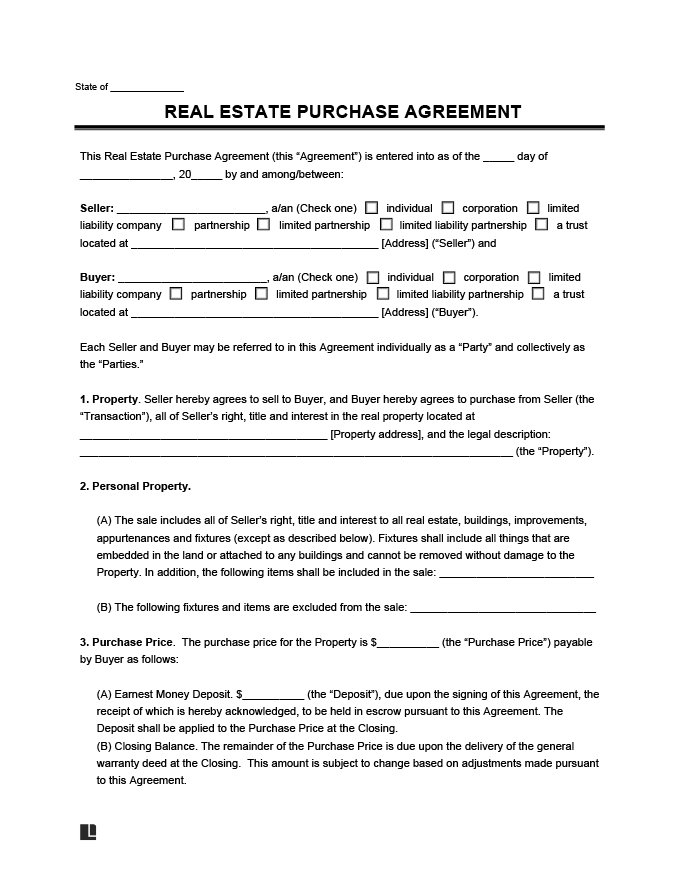

What Is a Real Estate Purchase Agreement?

A real estate purchase agreement is a legal contract outlining a property sale between you and a seller.

In real estate, you fill out the document and use it to negotiate the terms with the seller. Once both parties agree to the property sale for a specific price and contingencies, they sign it to lock in the terms. Often, you will pay an earnest money deposit to signal your commitment. From there, the parties can proceed with the next phases in the contract, including home inspections.

Our real estate purchase agreement template records all the details so you can make a real estate sale possible. Outline each party’s rights and duties and explain the steps necessary to complete the deal.

What to Know Before Writing a Real Estate Purchase Agreement

Before writing a real estate purchase contract, you should know key considerations to help your sale go smoothly.

Property Ownership & Legal Status

Gather important documentation about the property’s legal status for clarification:

- Deed: A deed shows the transfer of ownership of a property. Different types of deeds might apply to your purchase, such as a warranty deed showing a clear title or a quitclaim deed offering no title guarantees.

- Title report: A title report shows a detailed history of the property’s ownership. It identifies existing liens, judgments, or easements that could affect its title. It also verifies the chain of ownership from past owners.

- Property survey: A property survey defines the property’s boundaries, including the border between it and any neighboring parcels or private or public land. It confirms the property’s legal boundaries and prevents disputes over property lines.

- Zoning and land use restrictions: These define the legal use of a property based on local zoning laws. For example, a property in a residentially zoned area may be restricted from commercial use.

Financial & Informational Documents

The seller must also provide financial and informational documents for transparency. These include:

- Mortgage payoff statement: This statement highlights the amount remaining on the mortgage.

- Property tax records: These records show the taxes paid on the property and if any are outstanding.

- HOA documents: These documents provide information about the homeowners association to which the property is subject.

Earnest Money Deposits

An earnest money deposit shows your commitment to completing the sale. The amount typically ranges from 1% to 10% of the home’s price. It is held in escrow to protect the seller against potential withdrawal.

A contract outlines conditions for refunding the deposit, with contingencies allowing you to withdraw without penalty in certain situations. For example, property issues or financing failure may let you get your money back. If you back out without a valid contingency, you will forfeit the deposit.

Earned Interest

Any interest earned while in escrow typically benefits the buyer and is often applied to closing costs or the down payment.

Amendments & Addendums

Amendments modify the original real estate purchase agreement. They typically address unexpected changes or correct errors in the original contract. When you and the seller complete them correctly, they become legally binding.

Addendums are terms that are added to the purchase agreement and are not found elsewhere in the document. Contingencies are one type of purchase agreement addendum. Here are some common addendums within a real estate purchase agreement:

- Release of earnest money: States that a seller must release the earnest money deposit to you under certain conditions.

- Escrow holdback agreement addendum: Outlines the regulations for funds held in an escrow account.

- Closing date extension: Pushes the closing date, allowing the parties more time to prepare.

Do Contingencies Have to Be Addendums?

You don’t have to add contingencies as addendums. They can be part of the original real estate purchase agreement. In the initial contract, you may outline contingencies, such as the sale only going through upon seller financing approval or the sale of another home.

Disclosures

Disclosures in a purchase agreement provide you with information about potential property issues. The items outlined could impact the home’s value or legal mandates about specific safety or health problems. Some examples of disclosures include the following:

- Lead-based paint disclosure: Required for properties built before 1978.

- Property disclosure: Reveals any defects with the property, including foundational or structural issues.

- Boundary disputes disclosure: States if there have been prior boundary disputes.

- Death on property disclosure: Reveals if anyone has passed away on the property.

- Sexual offender disclosure: Discloses if a sexual offender has lived on the property.

- Environmental hazards disclosure: Clarifies if any environmental hazards exist that affect the property’s habitability.

- Condition of water/sewer systems disclosure: Reveals if the property’s water or sewer systems have issues.

Buyer Beware

When buying a home, it’s essential to understand that some states don’t require sellers to tell you about major problems with the property. This rule is known as “buyer beware” or “caveat emptor,” which means you’re buying the property in its current condition.

Safeguard your interests by seeking a property inspection. Examine the results closely and consider the answers to these questions:

- What kind of inspections do I need?

- Does closing the deal depend on the inspection outcomes?

- If the seller doesn’t make certain repairs, can I back out of the sale?

- If the inspection uncovers problems, when do they need to be fixed?

Buyer Beware States

Getting a detailed inspection is crucial, particularly in states that follow the “buyer beware” principle: Alabama, Arkansas, Georgia, North Dakota, Virginia, and Wyoming.

How to Write a Real Estate Purchase Agreement

Follow these steps to write a legally binding agreement. Or, save time and effort by using our real estate purchase agreement template. We guide you through each step and help you document all the important details.

1. Fill Out the Buyer’s and Seller’s Information

Write down the seller’s full name. Indicate if they are an individual or entity, such as a corporation, LLC, or trust. Provide the seller’s street address. Do the same for your own information as the buyer.

It’s quick and easy to add more buyers and sellers if necessary with Legal Templates’s real estate purchase agreement form.

2. Describe the Property

The description provides details about the property being sold, such as the physical address and identifying features. With our purchase agreement template, you can upload photos, a legal description, or other supporting documents. You can also specify if a related property is being sold.

3. Identify Real and Personal Property

Summarize what the real estate sale will include. The purchase includes all real property, buildings, improvements, appurtenances, and fixtures. You have the option to include additional personal property items in the sale.

You can choose whether to exclude certain fixtures and items from the sale. If you do, provide a list of those items so all parties are on the same page.

4. Provide the Purchase Price and Details

Fill in the agreed-upon purchase price for the property. Write the total amount of the earnest money or “good faith” deposit. At closing, the earnest money deposit shows as a credit toward the purchase price. Indicate how you will pay the seller, via cash or another method.

Payment Options

If you can’t pay with cash upfront, you may use a loan agreement or payment plan. If you’re close with the seller, a promissory note may suffice.

5. Describe Disclosures

You can specify seller disclosures, such as environmental hazards, flooding or drainage issues, etc. The seller must provide disclosures required by law. They should also give information about issues that may affect the property’s value or quiet enjoyment.

6. Write Assumption of Loan Details

State whether you will take over the seller’s mortgage. If yes, provide the name of the financial institution, the mortgage date, and the mortgage’s current balance. Also, indicate which party will pay the fees related to the mortgage transfer.

7. Identify Financing Contingencies

Choose your desired terms for the mortgage. Write whether you want the agreement contingent upon an appraisal with a value equaling or exceeding the purchase price.

Satisfaction of Mortgage

In some cases, the purchase and sales agreement might involve your assumption of the seller’s existing mortgage. If this applies, you must include provisions regarding the satisfaction of mortgage within the agreed-upon timeline.

8. Enter Sale Contingencies

State whether the purchase and sales agreement is contingent upon you selling a property. If yes, provide the street address of the property that must be sold first.

9. Fill in Representations and Warranties

Our real estate purchase contract provides for standard sellers’ representations and warranties regarding title, authority to sell, and the property’s non-violation of government rules, codes, permits, and regulations.

Our template lets you add as many seller representations and warranties as you’d like so you can capture all the seller’s promises in one place.

10. Provide Inspection Details

If you desire, our real estate purchase agreement ensures that the purchase is contingent upon the results of an inspection. You can ask the seller to fix or repair any unsatisfactory conditions. Choose whether to include a date by which the buyer and seller must agree on repairs.

11. Write Down Title Insurance Details

Choose who pays for the title insurance, who selects the insurance company, and whether you want to include any allowable exclusions or exceptions to the policy.

Provide the days the buyer has to notify the seller of any objections to the title after receiving the preliminary report. Enter the days the seller has to correct or address the complaints after receiving the buyer’s notice.

12. Enter Closing Details and Deliverables

Provide the date and location of the transaction’s closing. Identify which party will cover the closing costs.

Also, name the buyer and seller deliverables. Use our purchase and sales agreement template to specify what each party must provide for the sale to go through.

You can also decide whether you’re allowed to delay closing due to your lender requiring additional documentation or information. If yes, provide the number of days you can extend the closing.

13. Record the Property Possession Date

Provide the date the seller must deliver possession of the property. If the seller wishes to wait until certain conditions are met, ensure the listed date reflects this preference.

14. Identify Assumption of Leases

Write whether the seller is currently leasing the property. If yes, provide the name and date of the lease agreement as well as the name of the lessee.

15. Fill in Governing Law, Disputes, and Miscellaneous Information

Choose the state’s laws that will govern the sales and purchase agreement.

If there are disputes, choose whether the parties will resolve them through:

- court litigation

- binding arbitration

- mediation

- mediation then arbitration

You can include additional provisions to the purchase agreement.

16. Fill in Lead-Based Paint Disclosures

If the property was built before 1978, the seller must disclose the presence of known lead-based paint hazards.

As the buyer, you must initial and sign the lead disclosure warning. You must also acknowledge receiving a pamphlet titled “Protect Your Family from Lead in Your Home.”

Suppose an agent is involved in the transaction. In that case, they must initial and sign the lead disclosure statement, acknowledging the agent informed the seller of the seller’s obligations under 42 USC §4852d.[lt_source id=”1″]

17. Collect Signatures

Sign the document as the buyer and collect the seller’s signature. Proceed with the terms in the agreement, respecting contingencies that may cause the deal to become invalid.

Should I notarize my real estate purchase agreement?

Depending on your state, notarizing the purchase and sales purchase agreement might be required by law. You might consider notarizing the contract even if the law does not require it. This can help prevent fraud and support your legal rights if there is a dispute about the contract.