What Is a Profit and Loss Statement?

A profit and loss statement (P&L) shows how much a business earned and spent during a set period. It reveals whether the business made money or lost money. From there, it breaks down where revenue came from and how expenses affected the final result.

A P&L statement gives business owners a fast way to review performance and spot changes in revenue, expenses, and profitability across each reporting period. It’s one of the core financial statements and acts as a formal financial document that summarizes a company’s revenues and expenses over a given period. It usually starts with gross revenue at the top and ends with net income at the bottom line.

A P&L follows revenue recognition, matching, and accrual rules, so it records income when earned and expenses when incurred. That approach gives a clearer picture than cash alone and typically includes:

- Revenue from sales, service fees, commissions, rental income, or interest

- Major expenses such as costs of goods sold (COGS), raw materials, operating costs, selling, general and administrative (SG&A), marketing, wages, insurance, taxes, and interest

Public companies prepare profit and loss statements multiple times a year under generally accepted accounting principles/practices (GAAP). Smaller private businesses may take a lighter approach, but the statement still helps them understand their numbers and catch issues early.

A P&L statement is key for drafting a business plan, setting up an LLC operating agreement, or filing articles of incorporation.

Income Statement vs. Profit and Loss

An income statement and a profit and loss statement mean the same thing. Both show what a business earned, what it spent, and the final profit or loss for the period. Only the name changes.

| Term | What It Means | Who Uses It |

|---|---|---|

| Earnings Statement / Statement of Operations | Additional names for the same report. | Used by some organizations. |

| Profit and Loss | The everyday name used inside companies. | Managers, lenders, FP&A teams. |

| Income Statement | The formal name used in official reporting. | Accountants, auditors, regulators. |

No matter the term, the report follows the same structure:

- Revenue at the top

- COGS and gross profit

- Operating expenses and operating income

- Interest, taxes, and net income at the bottom

Operating income focuses on profit from core business operations, before interest and taxes are taken into account.

Companies prepare one document regardless of the label. The name may change, but the report still shows whether the business earned a profit and how it managed its costs.

Profit and Loss Statement vs. Balance Sheet

A profit and loss statement and a balance sheet serve different roles, even though both explain key parts of a business’s finances. A P&L covers a period of time, while a balance sheet captures a single moment. That timing shapes what each report shows.

A P&L focuses on performance:

- Revenue, expenses, and profit over the period

- A view of how well the business earned money and managed costs

A balance sheet focuses on financial position:

- Assets, liabilities, and equity at one point in time

- Insight into debt levels, working capital, and overall stability

These differences mean you get a fuller picture when you use both statements together. A P&L shows activity, while a balance sheet shows strength. Both statements also connect to the cash flow statement. Accrual accounting can show profit even when cash is tight, so comparing all three reports helps explain gaps between profit and actual cash available.

When to Rely on a Profit and Loss Statement

Use a profit and loss statement when you need a clear view of what the business earned and spent during a set period. It’s useful for monthly, quarterly, or yearly check-ins because it shows whether the business made a profit or recorded a loss.

A P&L also helps when you’re comparing different reporting periods. It shows how revenue and expenses shift over time, which is important for internal reviews and lender requests. It’s equally helpful when you want to break income into service lines or products to see which areas add the most value.

Common situations where a profit and loss statement helps include:

- Tax preparation and year-end reporting

- Loan applications that require margin visibility

- Investor reviews that require clear financial results

- Annual planning and forecasting for future spending

A P&L gives structure to all of these activities by showing where money came from and where it went. For startups and growing businesses, a regular P&L works alongside basic bookkeeping to keep financial performance organized and support smarter decisions as the company scales.

Benefits of Using a P&L

- Allows you to see how revenue and expenses change from one period to the next, so trends are more easily visible.

- Helps you catch rising costs or shrinking margins early.

- Makes it easy to spot overspending in payroll, admin, or marketing.

- Supports better pricing, budgeting, and cost control.

- Shows how well the business turns sales into profit by looking at margins. Tracking these margins over time gives a clear view of long-term profitability.

- Helps you identify issues before they escalate into larger financial problems.

How to Make a Profit and Loss Statement

When you write a profit and loss statement, you’re organizing the numbers that explain how your business performed during the period. These steps help you turn raw income and expense details into a clean, usable report.

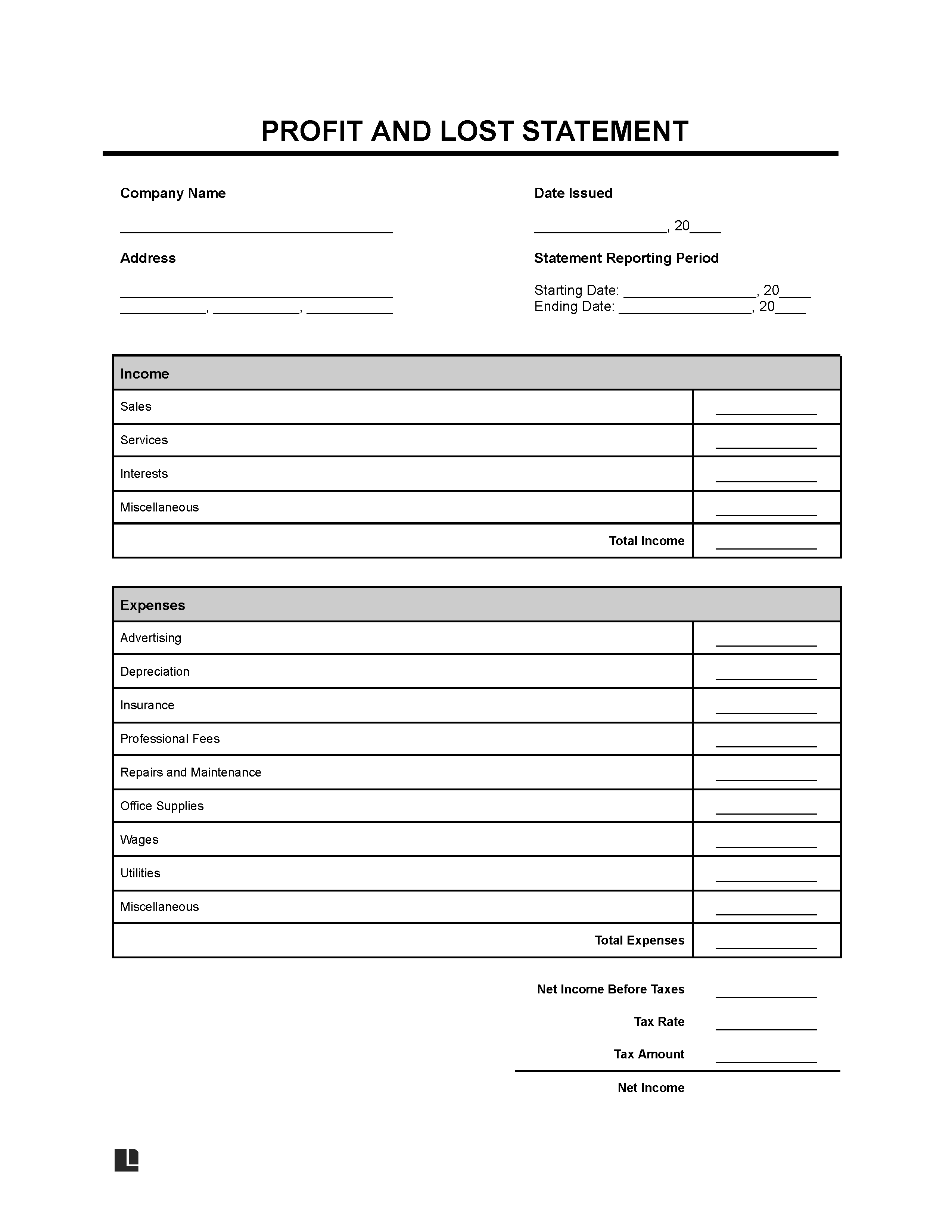

Whether you track income and expenses using our profit and loss template, a simple P&L template in a spreadsheet, or accounting software, the basic steps for building your P&L stay the same. You can also use our builder to easily customize your statement online and save or download it in PDF or Word. Many businesses still duplicate the layout in Excel or Google Sheets for internal tracking between formal reporting periods.

1. Enter Your Business Information

Start with the basics so the statement has context. Add your company name, business address, the date issued, and the reporting period. These details tell the reader exactly which timeframe the numbers represent. An accurate setup also ensures your bookkeeping records and financial reports stay aligned from month to month.

2. Record Revenue Sources

Next, list every source of income for the period. Include product sales, service income, interest, and any other revenue. Keeping these categories separate helps you see which activities brought in the most money.

3. List Business Expenses

Then, record all operating costs. Add items like advertising, depreciation, insurance, professional fees, repairs, office supplies, wages, and utilities. This step shows where money went and makes unusual cost increases easier to spot.

4. Calculate Net Income

Once income and expenses are listed, calculate your results. Subtract total expenses from total income to get net income before taxes.

Many businesses also calculate a subtotal for operating income so they can see results from ongoing operations before taxes and other non-operating items. Apply your tax rate, then subtract taxes. This gives you the final profit or loss for the period.

5. Generate Your Statement

With everything entered, you can compile the statement. Our editor formats each section for you, creating a clean document you can use for reviews, planning, or reporting. By writing your P&L in this order, you create a statement that’s easy to read and simple to verify. It gives you a clear record of the period and a structured financial report for planning, budgeting, or preparing year-end filings.

How to Read a Profit and Loss Statement

Reading a profit and loss statement starts at the top. Look at total revenue, then follow the numbers down to net income. This provides a quick overview of the business’s earnings and the amount remaining after expenses. To understand the story behind the numbers, review each section in order:

- Compare periods. Look at changes in revenue, COGS, SG&A, marketing, and payroll. This shows whether performance is improving or slipping.

- Check gross profit. See if COGS is rising faster than sales. Shrinking margins can signal pricing or cost issues. Rising cost of goods sold often signals higher supplier pricing, increased production waste, or issues in inventory control.

- Review operating expenses. Identify overhead that’s growing too quickly.

- Analyze EBITDA. This shows operating performance before interest, taxes, and non-cash items.

- Look at depreciation and amortization. These entries reveal the long-term cost of assets.

- Study margins. Review gross, operating, and net margins to see how efficiently revenue turns into profit.

- Compare against peers. Benchmarking helps you understand how your results stack up in the industry.

- Use horizontal analysis. Tracking changes over time makes trends easier to spot.

- Calculate ratios. Pair P&L totals with balance sheet data to find return on equity (ROE), return on assets (ROA), and other indicators.

Remember that profit does not equal cash. Accrual accounting can show a profit even when cash is tight. That’s why a profit and loss statement works best when you review it alongside the balance sheet and cash flow statement. Together, they give you a complete picture of financial health.

Example Profit and Loss Statement

Here’s a completed profit and loss statement so you can see how each section looks when filled out. This accounting profit and loss statement example uses simple business details and rounded figures to show how income, expenses, and net income come together on the final document.

PROFIT AND LOSS STATEMENT

Company Name Date Issued

BrightPath Consulting LLC 01/15/2025Address

1024 Market Street

Denver, CO 80202Statement Reporting Period

Starting Date: 01/01/2024

Ending Date: 12/31/2024Income

Total Amount $485,000

Expenses

Total Amount $312,400

Net Income Before Taxes $172,600

Tax Rate 22%

Tax Amount $37,972

Net Income $134,628

Sample Profit and Loss Statement

View a sample profit and loss statement to see how the finished document looks. This free template gives you a professional structure without requiring paid accounting tools. You can use this example as a reference when filling out your own. Customize and download our template for a profit and loss statement in Word or PDF.

This profit and loss statement template is designed for accurate reporting, trend analysis, and lender-ready financial reviews.