The costs and fees associated with filing a quitclaim deed in New York can vary based on several factors, including the property’s location, any applicable county recording fees, and additional expenses for legal advice or service facilitation. Understanding these costs is crucial for anyone looking to use a quitclaim deed in New York, ensuring a smooth and legally compliant transfer of property rights.

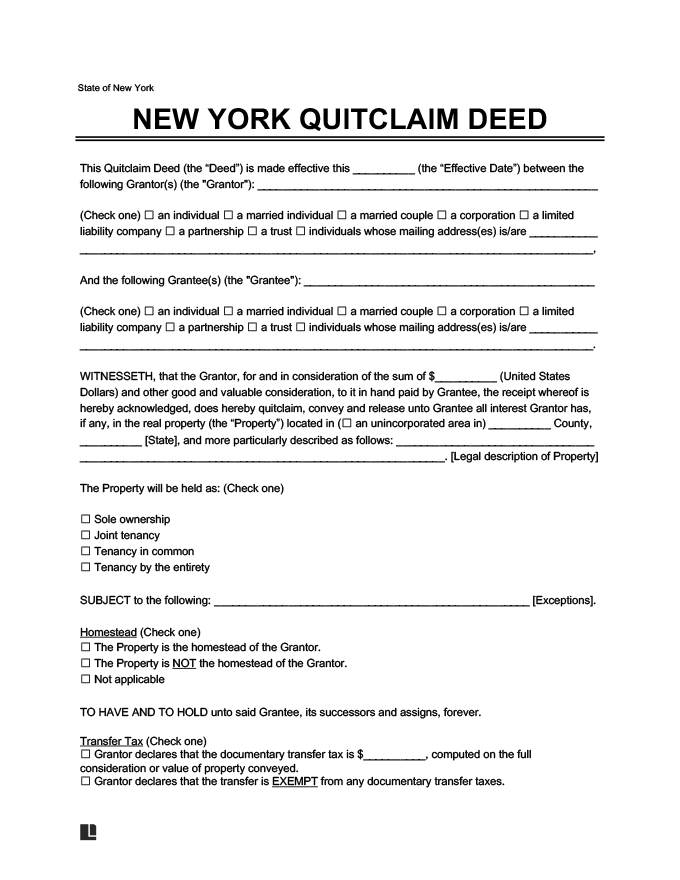

In New York, grantors — or the people giving property in a quitclaim deed — must fill out multiple tax forms to present alongside their completed deed for filing. Transfer tax, gift tax, and capital gains tax may all apply.

Filing Fees

Quitclaim deed filing fees in New York vary depending on the specific county. But generally, the fee for filing a quitclaim deed form is $125 for residential or farmland and $250 for all other property types. Find the New York county clerk’s office for the county in which the property exists to look up the exact filing fees for your purposes.

Taxes

Those involved in a New York property transfer must complete forms TP-584-NYC and RP-5217NYC for property located in New York City and TP-584 and RP-5217 for properties in counties outside New York City.

1. Documentary Transfer Tax (DTT)

A New York transfer tax applies when the consideration of the property to be transferred exceeds $500. Some types of property transfers are tax-exempt, such as gifts and bequests, transfers into trusts, and transfers that merely change the character of the property, such as adding or removing a spouse.

If you are unsure whether your quitclaim deed is tax-exempt, you should consult a property attorney.

Who Pays the Transfer Tax?

The grantor generally pays the transfer tax, although the grantee can pay it if a signed contract between the two states they will. If the grantor doesn’t pay or is exempt from the transfer tax, the grantee must then pay it.

A mansion tax, or additional base and supplemental taxes for properties exceeding certain values above $1 million, is entirely the responsibility of the grantee. If the grantee does not or is exempt from applicable additional and supplemental mansion taxes, then the grantor must pay them.

Exemptions to Transfer Tax

Exemptions from the New York transfer tax include:

- A US government entity

- A New York State entity

- A foreign government, or its representative, when the property will be used exclusively for diplomatic or consular purposes

If a government entity transfers property to a non-government entity, the non-government entity must file a return and pay the transfer tax.

Tax Rates

The tax rate is $2 for each $500 of consideration. There are additional taxes where the consideration exceeds certain amounts starting at $1 million, including:

- When consideration of a residential property exceeds $3 million, an additional $1.25 for each $500, or fractional part thereof in base tax applies.

- When consideration for a non-residential property is $2 million or more, an additional $1.25 for each $500, or fractional part thereof in base tax applies.

- When consideration of a residential property is $2 million or more, a supplemental tax with an incremental rate between .25% and 2.9% based on the purchase price applies. Exact tax rates can be found in Form TP-584-NYC-I, which also gives Instructions for Form TP-584-NYC.

2. US Gift Tax (Form 709)

There is no New York-specific gift tax, so parties involved in a New York quitclaim deed must only consider the federal gift tax. Using IRS form 709, the grantor, who pays the gift tax unless the grantee agrees to pay in writing, can find the amount they may owe in gift tax. A gift tax only applies if the full monetary value of the property is not received in return for its transfer.

3. Capital Gains Tax

In New York, capital gains are taxed as personal income tax. Federally, capital gains tax applies to a grantee who later sells a gifted property for more than the adjusted basis amount (IRS Topic No. 409). IRS Publication 551 helps grantees calculate the adjusted basis amount of property gifted to them.