LLC Operating Agreements – By State

When you’re ready to create an operating agreement for your LLC, you can select your state below to learn more about state-specific laws. Then, use Legal Templates’s questionnaire to draft your own and establish your company’s governance procedures.

- Alabama

- Alaska

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- District of Columbia

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming

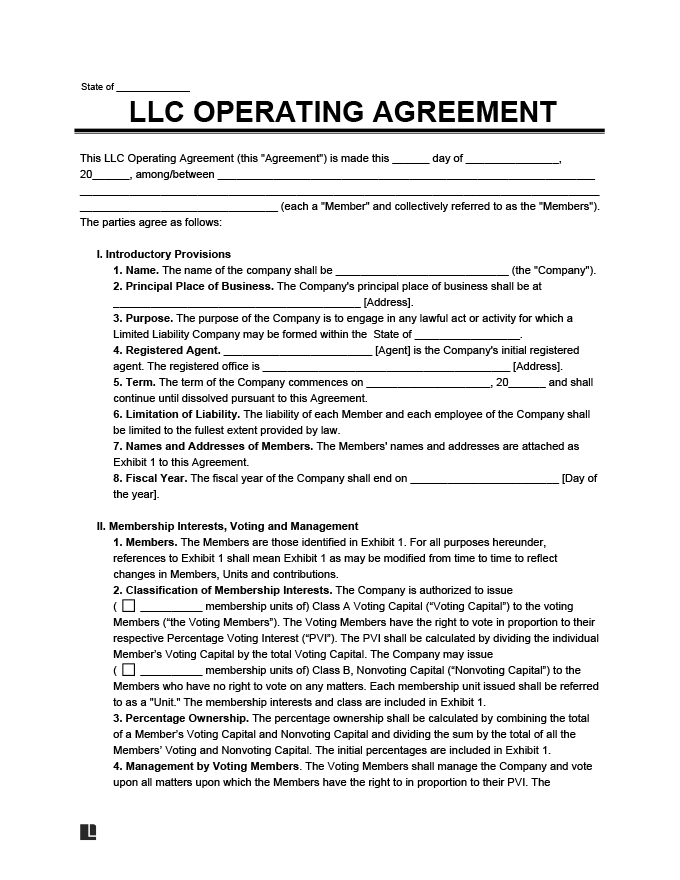

What Is an LLC Operating Agreement?

An LLC operating agreement outlines how a limited liability company is structured and managed. It gives clear guidelines for governance, ensuring smooth operations and preventing disputes.

This document also clarifies that the LLC is separate from its owners. Any actions taken under the LLC are distinct from individual actions, preventing owners from personal liability.

Without an operating agreement, an LLC is governed by default state laws. These rules can be enough for some companies, but they may restrict the growth of others. It’s best to write your own LLC operating agreement to ensure your company operates how you want it to.

LLC Operating Agreement vs. Articles of Organization

An operating agreement explains how an LLC operates, while articles of organization formally establish the LLC. The operating agreement remains internal, and the articles of organization get filed with the Secretary of State or equivalent office. Articles of organization are an LLC’s version of articles of incorporation.

Do I Need an Operating Agreement for My LLC?

Some states legally require LLCs to have an operating agreement to remain compliant:

- California (CA Corp Code § 17701.13)

- Delaware (6 DE Code § 18-101)

- Maine (31 ME Rev Stat § 1531)

- Missouri (MO Rev Stat § 347.081)

- New York (NY LLC L § 417)

All other states do not have official requirements for LLCs to write and maintain an operating agreement in their records. However, it’s highly recommended to have an LLC operating agreement even when it’s not legally required. By writing an LLC operating agreement, you can:

- Create a clear structure for running the company

- Separate the company from its owners (for liability)

- Clarify ownership, roles, and decision-making authority (confirm roles with a certificate of incumbency)

- Assign voting rights

- Detail the processes for dissolving or existing the LLC

- Outline the duties and responsibilities of each member

- Prove to third parties (like lenders) who has the authority to act on the business’s behalf

Types of LLC Operating Agreements

There are two main types of LLC operating agreements: single-member and multi-member. The type of LLC operating agreement template you need will depend on the number of owners the company has.

| Single-Member LLC Operating Agreement | Multi-Member LLC Operating Agreement |

|---|---|

| For LLCs with a single owner | For LLCs with more than one owner |

| Less complex terms because one owner maintains control | More complex terms for decision-making and dispute resolution |

Single-Member LLC Operating Agreement

If you are the only owner of the company, then you will likely need a single-member LLC operating agreement. These agreements are generally less complex than those of multi-member LLCs, as all authority typically resides with one member, and there is less risk of internal conflict.

Single-member operating agreements are also used for LLCs that are a wholly-owned subsidiary of another legal entity, such as another LLC or a corporation.

Multi-Member LLC Operating Agreement

LLCs with more than one owner will need a multi-member LLC operating agreement. These documents are generally more complex due to the various issues that arise when multiple parties have an interest in the company.

For example, multi-member operating agreements often have terms that define each party’s membership interest in terms of outstanding units or percentages. Additional concepts that a multi-member LLC operating agreement can address include:

- Adding or removing members from the company

- Selling or transferring a member’s ownership interest

- Voting on key business decisions

- Establishing a priority for distributions or profit sharing among members

- Making additional capital contributions to support the business

- Dissolving the company

Members should consider how these terms within a multi-member LLC operating agreement can impact their individual rights and duties as owners.

Access each type of LLC operating agreement below and use our guided form to customize the template to fit your specific business needs.

Single Member LLC

This document governs the operations of an LLC with only one member (owner).

Multi Member LLC

This agreement is for LLCs with two or more members, each of whom holds a membership interest in the company.

Member-Managed vs. Manager-Managed LLC Operating Agreements

Legal Templates’s operating agreement form also lets you specify whether your LLC will be member-managed or manager-managed. A member-managed LLC has all members participate in decision-making. Meanwhile, a manager-managed LLC delegates authority to one decision-maker.

How to Create an Operating Agreement for Your LLC

Creating an operating agreement for your LLC can ensure all members understand its structure and processes. Learn how to write an LLC operating agreement below.

Step 1 – Add the Company Information

Start by writing basic company information, including the:

- Company name

- State of registration

- Tax classification (partnership, S-corporation, or C-corporation)

- End of the LLC’s fiscal year

- Whether the LLC will be member-managed or manager-managed

Step 2 – Name Your Registered Agent

A registered agent receives official communications from government bodies on behalf of your LLC. Your registered agent can be a member of your LLC, but they’re often a third party to ensure privacy and compliance with state laws.

Step 3 – Provide Member Details

Record essential details for each LLC member:

- Full legal name

- Number of membership units or ownership interests

- Class of membership units owned (for example, Class A or Class B)

- Percentage of voting capital/voting power

- Percentage of total capital owned

- Admission date into the LLC

- Consideration that the member paid (cash, assets, etc.)

Step 4 – Record Voting Procedures

Outline the details for voting procedures, including the following:

- Whether a unanimous or majority-in-interest (more than 50% of voting units) vote is required to approve a member’s transfer of ownership

- Whether a unanimous or majority-in-interest vote is required to admit new members

- Whether a unanimous or majority-in-interest vote is required to dissolve the LLC

- The percentage of voting members needed for a quorum

- How voting members can decide on other matters (unanimous, majority-in-interest, or ⅔ majority-in-interest)

Step 5 – Write Additional Terms & Final Details

Write any additional terms as you see fit. For example, you can stipulate that the members will act in good faith and in the best interests of the LLC.

Finish the agreement by adding the LLC’s principal place of business and the date that the agreement will go into effect. Have all members sign the contract so they can activate the document and be bound by its terms.

Does an LLC Operating Agreement Need to Be Notarized?

An operating agreement for an LLC does not need to be notarized. As long as it’s signed by all members and contains legal terms, it will be enforceable. However, seeking notary acknowledgment can help enhance the document’s validity and increase its legitimacy in the event of a dispute.

Step 6 – Amend as Needed

Over time, you may need to amend the terms of the operating agreement due to changes within the company. Some changes you may want to make include:

- Adding or removing members

- Obtaining new investments or financing

- Updating business purpose

- Revising the management structure

- Making new policy changes

- Clarifying dissolution or buyout terms

To update the agreement, you should use an amendment to the LLC operating agreement, which formally documents any changes to the original terms. Date and attach all amendments to the original contract to guarantee enforceability.

Planning for a member exit? A cross-purchase buy-sell agreement lets the remaining members buy out a departing owner directly, rather than having the company handle the purchase. It’s often used alongside an operating agreement to set clear buyout terms. You can review how it works and create your own cross-purchase agreement here.

What to Include in Your LLC Operating Agreement

Consider other provisions present in Legal Templates’s operating agreement form to ensure you complete a comprehensive document:

- Indemnification: A hold-harmless statement from the company.

- Profit and loss distributions: Methods for sharing profits and losses among LLC members.

- Member roles and responsibilities: Duties for each member (supplying new capital, engaging in business deals, etc.)

- Organization expenses: A statement clarifying that the LLC will pay for company expenses.

- Salaries: A statement clarifying that members won’t receive a salary (unless approved via a majority-in-interest vote).

- Dispute resolution: A statement proclaiming that any disputes will be resolved via arbitration or another method of the members’ choice.

Sample LLC Operating Agreement

Are you wondering what an operating agreement looks like for an LLC? View our free sample to learn what terms to include. Then, use our guided form to customize your own. Download a copy as a PDF or Word file for internal storage in your company’s records.

What Happens After Writing an LLC Operating Agreement?

Once all members sign the LLC company agreement, provide each member with a copy for their records. You may also want to have copies available at the following locations:

- LLC’s legal counsel

- LLC’s registered agent

- LLC’s principal place of business

Banks, investors, and other parties may also require a copy of the operating agreement before approving funding.

LLC operating agreements often include sensitive business information. To protect your business, only share essential elements with third parties as needed. If sensitive information is included, consider using a non-disclosure agreement to safeguard your company’s confidentiality. It may also be necessary to redact specific details before providing a copy to outside parties.