What Is a Partnership Agreement?

A partnership agreement is a written contract that sets the rules for running a partnership. It explains how two or more people or entities will operate a business together and share its profits and losses.

Partners may bring different things to the business, such as money, property, labor, or skills. The agreement puts those details in writing. It can cover how partners make decisions, divide profits, manage responsibilities, handle disputes, and respond when someone leaves the business.

Without a written agreement, state law may decide key terms for the partnership. Many states follow the Uniform Partnership Act (UPA) or the Revised Uniform Partnership Act (RUPA), which include default rules for profits, losses, and management rights. Those rules may not match the deal the partners actually made.

Before creating an agreement, it can help to review the advantages and disadvantages of a partnership to see how the structure fits your business plans.

Types of Partnership Agreements

The right partnership agreement depends on the partnership you’re building. Ownership, management, and liability can all work differently. These are the most common options:

General Partnership Agreement

A general partnership agreement is for two or more partners who jointly own and run a business. It often works best when the partners want to manage the business together and share day-to-day responsibility, profits, and liability.

General Partnership Agreement Template

Use our general partnership agreement to outline the terms of your business partnership.

Limited Partnership Agreement

A limited partnership agreement is for a business with at least one general partner and one limited partner. The general partner runs the business and can be personally liable for its debts. Limited partners are passive investors whose liability is limited to the amount they contribute to the business.

Limited Partnership Agreement Template

Outline all the key information of a partnership that has general and limited partners.

Limited Liability Partnership Agreement

A limited liability partnership agreement is for a partnership that gives partners some personal liability protection, depending on state law. Partners can often stay involved in management while receiving that protection.

Limited Liability Partnership Agreement Template

Use this template to detail the key information if your partnership will have members with limited liability.

Real Estate Partnership Agreement

A real estate partnership agreement is for two or more people who plan to buy, own, manage, or invest in property together. It can define each partner’s contributions, ownership share, responsibilities, and how profits or sale proceeds will be divided.

Real Estate Partnership Agreement Template

If you're looking to go into a partnership to buy or manage real estate then detail the key elements in our Real Estate Partnership Agreement.

50/50 Partnership Agreement

A 50/50 partnership agreement is for two partners who want to share ownership or economic interests equally. As the US Chamber of Commerce explains, partners should plan for decisions where neither side can make the call alone.

50/50 Partnership Agreement Template

Use this template if you want to equally share all profits and losses with a partner.

Partnership Dissolution Agreement

A partnership dissolution agreement is used when partners formally end a partnership. It can document how the business will wind down, how remaining matters will be handled, and what happens next.

Dissolution Agreement Template

Use our partnership dissolution agreement to protect your interests and assets and to provide clarity and protection for all parties involved.

Legal Templates offers partnership agreement templates for each of these structures, so you can choose the document that matches the business you’re building.

Is a Partnership Agreement the Same as an Operating Agreement?

No. A partnership agreement is for partnerships, while an LLC operating agreement is for LLCs. Ensure you use the right document to adequately cover key ownership, management, and decision-making terms for your entity.

How to Write a Partnership Agreement

Learning how to write a business partnership agreement helps you build terms around the way your partnership will actually operate. Cover the partners, contributions, money rules, decision-making, and future changes. Follow these steps to write a comprehensive agreement:

1. Add the Partnership Details

Start by identifying the partnership and the people behind it. Include each partner’s name, the partnership name, the formation state, and the main business address. Then, add when the partnership begins, whether it will end on a set date, and what the business will do.

2. List What Each Partner Will Contribute

Explain what each partner is bringing to the business. As the IRS notes, contributions can include money, property, labor, skills, or other non-cash support. Then, state whether each partner will contribute cash, non-cash assets, or both. Note when those contributions are due, too.

3. Decide How Money Will Be Handled

Partners should know exactly how money moves through the business. Set clear rules for how the partnership will earn and divide funds. Cover the following information:

- How profits and losses are shared: Choose an equal split, a split based on contributions, or another arrangement.

- When partners can take profits: Allow payouts on request, require partner approval, or set a regular schedule.

- Whether partners receive salaries: State if any partners will be paid for their work.

- Who handles key money decisions: Add the fiscal year, who can approve bank withdrawals, and whether partner accounts earn interest.

Make sure the agreement’s profit, loss, and capital-sharing terms match the partnership’s tax reporting on Form 1065.

4. Set the Rules for Running the Partnership

Decision-making rules shape who can speak and act for the business. Use this section to define each partner’s authority, when approval is required, and which major choices need full agreement. Also, state whether the partnership can bring in new partners later.

While one partner can have sole decision-making authority, shared approval may work better for major business choices. It helps keep key decisions balanced and gives all partners a voice in the direction of the partnership.

5. Explain How Records and Reports Will Work

Partners should know where to find important business records and when to expect financial updates. State where the partnership’s books will be kept, who can review them, and whether a partner’s representative may access them too.

Then, set expectations for financial reporting. For example, the agreement may require yearly financial statements and allow audits when the partners approve one.

6. Plan for Partners Leaving or Being Bought Out

Partner exits can change the whole business, so set the rules in advance. Explain what happens if a partner withdraws, retires, is removed for wrongdoing, or dies. Make sure the agreement covers:

- Whether the partnership continues: State if one partner’s exit ends the business or if the remaining partners can keep it going.

- Whether a buyout happens: Decide if the remaining partners must purchase the leaving partner’s interest.

- How the buyout price is set: Choose a valuation method before a partner leaves, retires, or dies. In one New Jersey case, a court enforced the agreement’s valuation method even though one side argued the interest was worth much more.

- When the buyout gets paid: State whether interest applies and when payment is due.

- How much notice is required: Set notice periods for retirement and buyouts.

Set the buyout process early, while partners are more likely to agree on fair terms. That way, the next steps are already clear if a partner leaves.

If you want a separate plan for what happens to a partner’s ownership interest when they leave, retire, or die, use a buy-sell agreement.

7. Decide How to End the Partnership or Handle Disputes

Explain how the partnership can voluntarily end and how many partners must agree. Courts may hold partners to these rules if one tries to dissolve the business without the approval the agreement requires.

Then, set a process for disputes. If partners will use arbitration, say so and name where it’ll take place and how the cost of arbitration will be allocated among the parties. For example, the agreement may send disputes to arbitration in a specific city or state and require the parties to equally share the arbitration fee.

8. Review and Sign the Agreement

Give the agreement one final review before it takes effect. Check that the terms match what the partners agreed to, then have every partner sign it.

If partners later change the agreement’s terms, they may need a partnership agreement amendment to record the update in writing.

Partnership Agreement Example

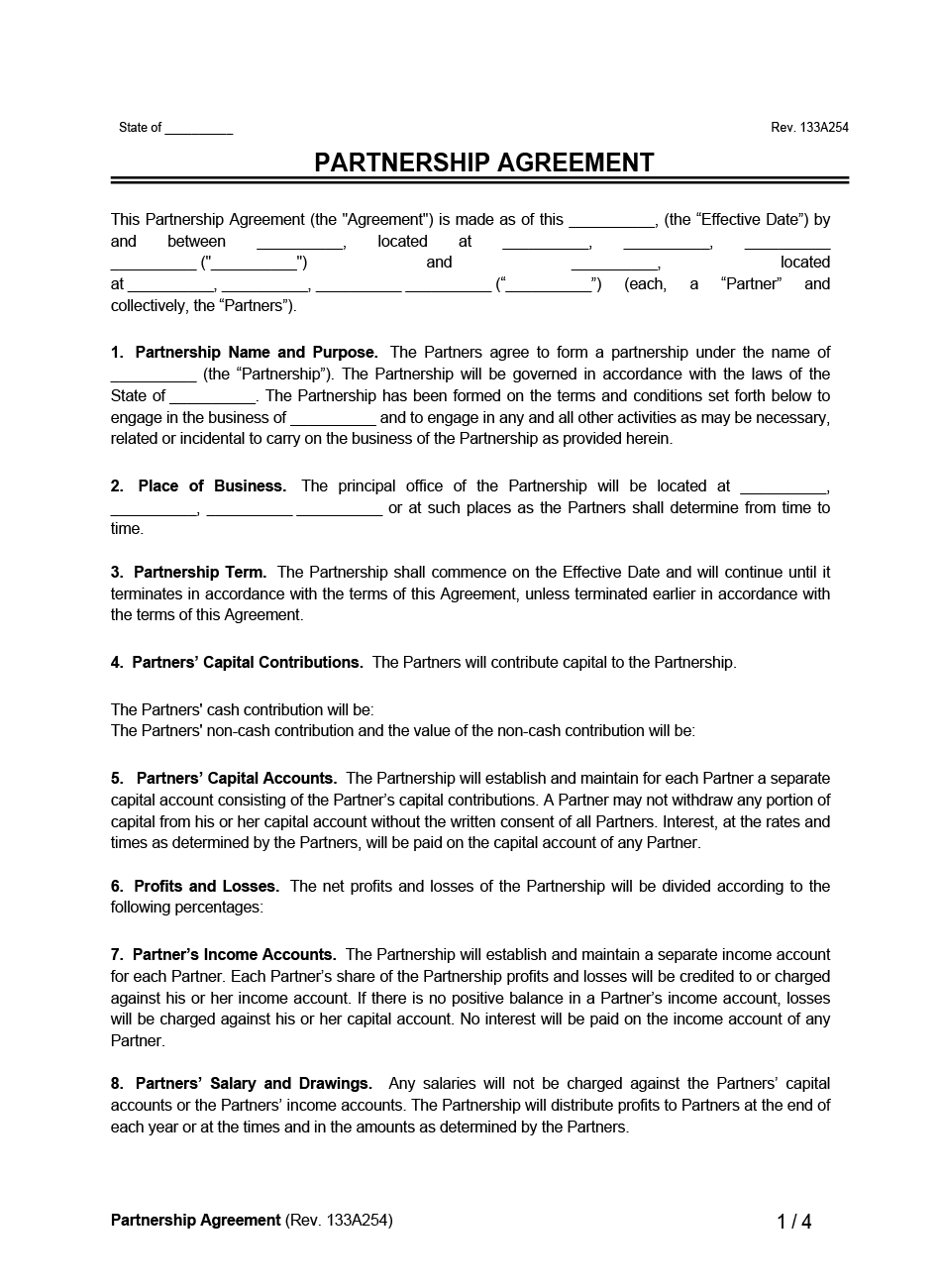

Here’s an example of how the first page of a completed partnership agreement may look. It uses a two-partner business in Alabama and follows the same wording and structure as our business partnership agreement template. View the sample below to see the full document layout.

State of Alabama

PARTNERSHIP AGREEMENT

This Partnership Agreement (the “Agreement”) is made as of this October 15, 2026, (the “Effective Date”) by and between Jordan Ellis, located at 125 Oak Street, Birmingham, Alabama 35203 (“Jordan Ellis”) and Maya Patel, located at 480 Pine Avenue, Huntsville, Alabama 35801 (“Maya Patel”) (each, a “Partner” and collectively, the “Partners”).

- Partnership Name and Purpose. The Partners agree to form a partnership under the name of Ellis & Patel Event Rentals (the “Partnership”). The Partnership will be governed in accordance with the laws of the State of Alabama. The Partnership has been formed on the terms and conditions set forth below to engage in the business of renting event furniture and décor and to engage in any and all other activities as may be necessary, related, or incidental to carry on the business of the Partnership as provided herein.

- Place of Business. The principal office of the Partnership will be located at 220 Market Street, Birmingham, Alabama 35203, or at such places as the Partners shall determine from time to time.

- Partnership Term. The Partnership shall commence on the Effective Date and will continue until it terminates in accordance with the terms of this Agreement, unless terminated earlier in accordance with the terms of this Agreement.

- Partners’ Capital Contributions. The Partners will contribute capital to the Partnership.

The Partners’ cash contribution will be:

- Jordan Ellis, $20,000

- Maya Patel, $20,000

The Partners’ non-cash contribution and the value of the non-cash contribution will be:

- Jordan Ellis, event inventory and storage equipment valued at $8,000

- Maya Patel, delivery van and booking software setup valued at $8,000

Partnership Agreement Sample

View the partnership agreement contract sample below to see how partners can fill in key details, like the business purpose, location, term, and contributions. Then, customize our simple partnership agreement template and download it in Word and PDF.