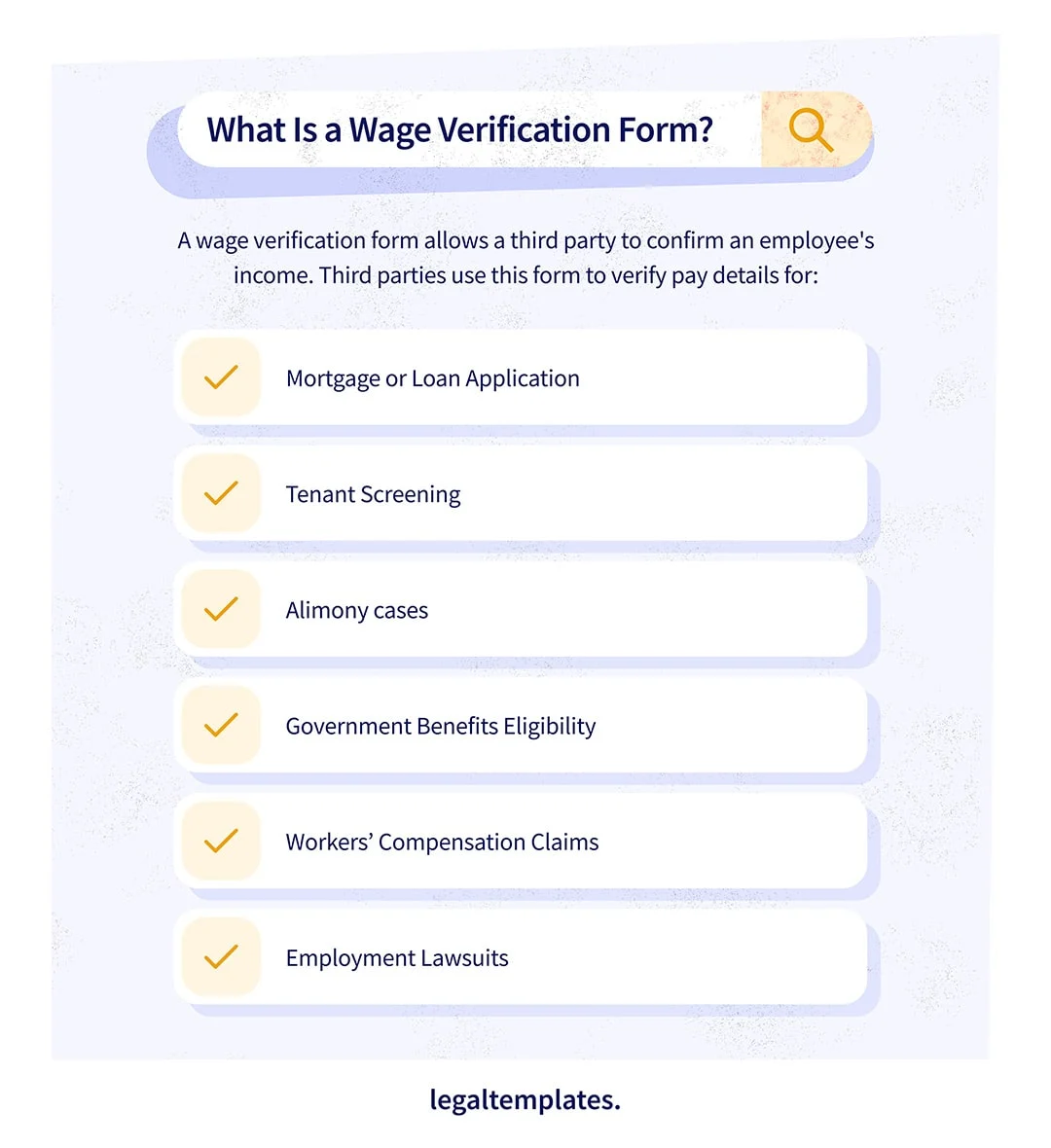

What Is a Wage Verification Form?

A wage verification form is a compensation verification document that confirms an individual’s income for legal or financial purposes. It may also be called an income certification form, proof of earnings form, or earnings verification form.

Third parties, such as child support agencies, lending institutions, potential employers, and landlords, use wage information forms to determine an employee’s financial stability. They study their findings to determine whether they want to approve an application for child support adjustment, a loan, employment, or a lease.

Legal Templates offers a wage verification form template to help third parties streamline the verification process. You can easily use our template to request income details from an applicant’s employer.

Employees must give consent for wage verification, so be sure to include a section for employee approval in your form.

What Are Common Uses of a Wage Verification Form?

Determining child support is one of the most common reasons for wage verification. The state and local Department of Health and Human Services (DHHS) often issue this form to determine the amount a non-custodial parent should pay for child support and living expenses.

While child support determination is the most common use for a wage verification form, it has many other uses.

Mortgage or Loan Applications

A mortgage lender or bank may request wage verification from a potential borrower as part of the loan application process. They use the form to verify income stability and establish whether the applicant can meet the repayment terms of the loan agreement.

A wage verification form helps lenders make informed lending decisions, reducing the financial risks associated with loan approvals.

Tenant Screening

A landlord or property manager may use a wage verification form to screen tenants during the rental application. The form lets them assess the potential tenant’s ability to pay rent and fulfill other requirements under the lease agreement.

If an employee asks an employer directly, an employer can fill out an employment verification letter to show that the employee has reliable income and can be a good tenant.

Alimony Cases

Courts handling alimony cases may request wage verification forms to establish the paying spouse’s financial capacity. Alternatively, the court may request the form to determine the income level of the spouse receiving alimony or support. A wage verification form from an employer allows the judge to calculate a fair alimony amount based on the actual income of both spouses in the case.

Government Benefits Eligibility

Wage verification is crucial for helping government agencies establish eligibility for benefits like unemployment and food assistance. The form provides critical income details to ensure eligible individuals or families receive benefits. Such forms provide accurate income reporting for the government agency, ensuring fairness and preventing fraud.

Insurance Claims

An insurance company may need to verify the claimant’s income to process disability, life insurance, workers’ compensation, and other claims. A wage verification form proves the value of lost wages and establishes accurate financial information for a fair insurance payout.

Workers’ Compensation Claims

Wage verification is especially crucial for workers’ compensation claims, as the injured worker can receive benefits for lost wages. The form ensures workers receive appropriate compensation for lost wages due to workplace injuries based on their actual income.

Employment Lawsuits

Employment lawsuits often require wage verification, especially in disputes involving unpaid wages, wrongful termination, and discrimination. A wage verification form provides evidence of any income discrepancies to ensure fair compensation.

Are Wage Verification Forms Always Required?

Not all lenders, landlords, or other third parties require a wage verification form as proof of income. For instance, self-reported income in the form of tax returns or pay stubs may be sufficient for a landlord with a short-term rental property instead of contacting an applicant’s former employer.

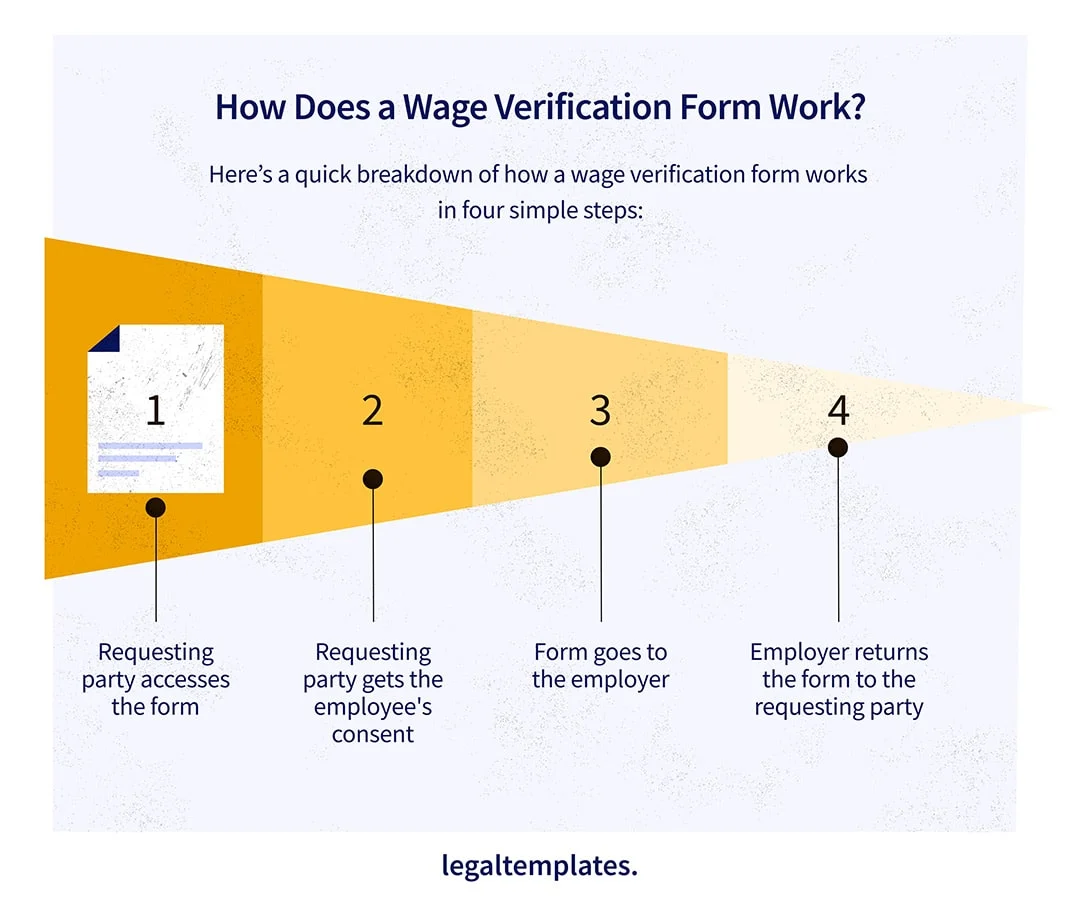

How Does a Wage Verification Form Work?

Wage verification forms are relatively straightforward. Understand how the process works by reading the below steps.

1. Requesting Party Accesses the Form

A third party who needs wage details initiates the process. They start by accessing a wage verification form, like the one from Legal Templates. Here, they provide all preliminary information, including the verifying party’s name, address, and contact information. They can also state the purpose of the verification and whether it has an expiration date.

They should also provide the name of the person whose wage is being verified and their employer. Also, they need to list instructions for the verifying party on how to return the document. As the requesting party, you can easily complete step one directly in our template.

2. Requesting Party Obtains Employee’s Consent

Before you can submit a wage verification form to the employer, you must have the employee’s written consent—this is non-negotiable.

The employee should give explicit consent, such as “I authorize my employer, Example Company, to release my salary, commission, and bonus information to Requesting Party.” This way, it’s clear that the employee is authorizing that particular employer to release their wage information to the requesting party.

The employee must give their consent voluntarily and sign the consent to confirm their understanding.

3. Form Goes to the Employer

Once the requesting party receives the employee’s written consent, the requesting party sends the verification form to the employer. The employer fills out the wage information on the form, including:

- employee name

- job dates

- status (full-time, part-time, etc.)

- pay frequency

- wage amount

- overtime

- additional compensation (bonuses, commission, etc.)

- employer contact info

The employer should acknowledge the certification statement on the form to confirm all the information they provided is true and updated to the best of their knowledge. Then, they can finish filling out the form by adding their signature.

4. Employer Sends Form to Requesting Party

Once the employer fills out their part of the form, they can return it by following the instructions that the requesting party provided. Ideally, they will send it directly to the requesting party, as it can help them make an informed choice for actions like loan approval, tenancy approval, or establishment of child support payments.

How Legal Templates Helps With Wage Verification

Legal Templates provides individuals or businesses who need wage verification with quick and easy access to customizable forms. Our platform allows you to create, customize, and complete a printable wage verification form quickly and reliably.

Using our stress-free digital platform, third parties seeking wage verification can quickly fill in their information, print the form, and send it to the employee for consent before forwarding it to the employer. The employer will supply the requested information, with the employee’s consent, and return it to you.

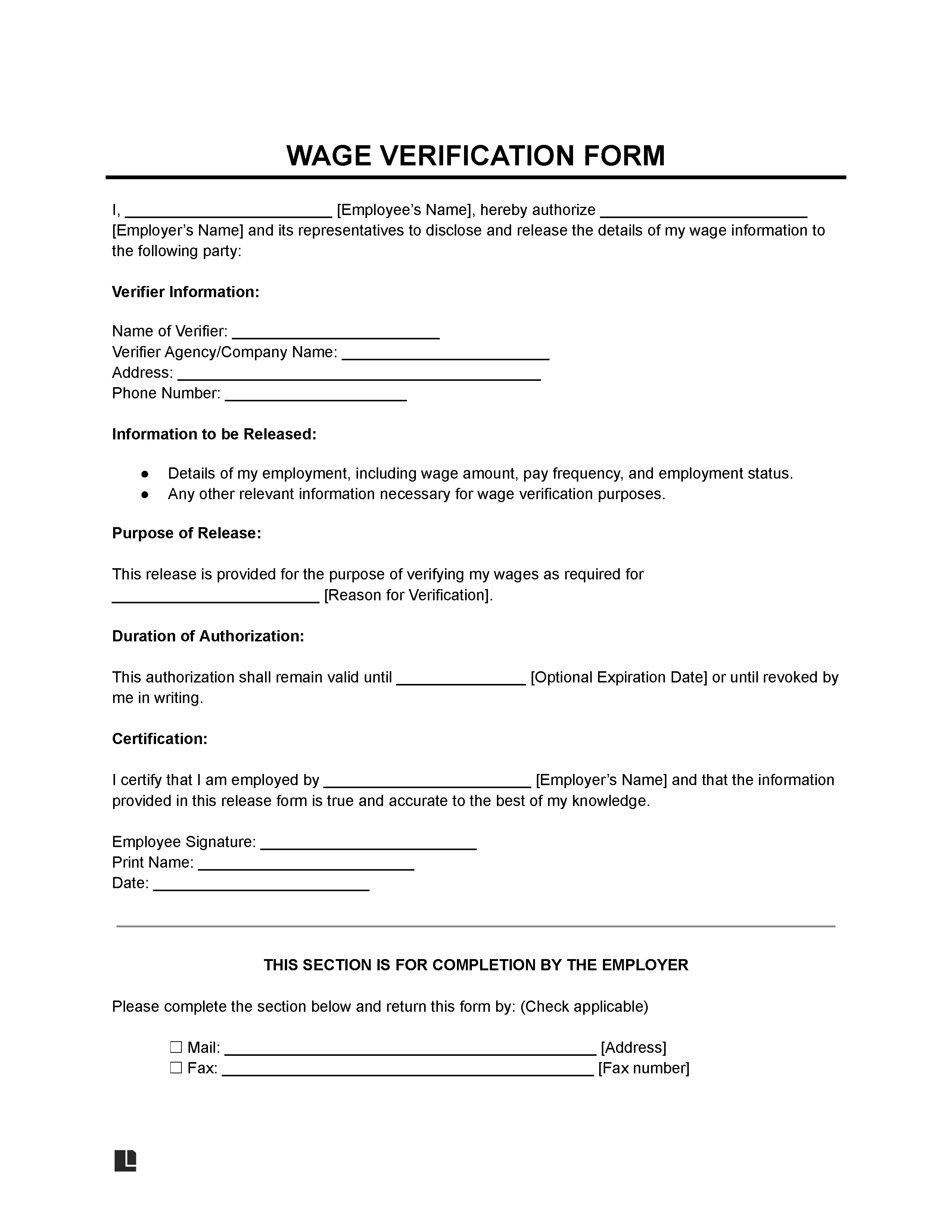

Wage Verification Form Sample

Below is an example of a wage verification document so you can study its format and structure. When you’re ready, create your own via our wage verification form template.

Frequently Asked Questions

What happens if the wage verification information is incorrect?

Incorrect wage information can stall or nullify an approval process. A potential lender, landlord, or other third party will need to take additional steps to confirm the correct information, or they may discontinue the process altogether.

Can wage verification be used for multiple purposes?

Wage verification can be used for many purposes. However, it’s best for the requesting party to gain explicit consent from the employee if they need to use a wage verification for different purposes.

What if an employer refuses to complete the wage verification?

If an employer refuses to complete a wage verification, they could compromise the employee’s ability to secure a loan, housing, or other services. The employer may need to pay fines or other penalties if their refusal violates a law or court order. However, the employer can refuse the request if it doesn’t come from a government agency or court order.