What Is a Revocable Living Trust?

A revocable living trust helps you manage your assets during your lifetime and decide how they’ll be distributed after you pass away. It takes effect while you’re alive and can be changed or canceled whenever your circumstances shift. The trust only becomes valid once you transfer assets into it.

If you can’t manage your finances, your appointed trustee can step in to handle the assets in the trust. Their authority applies only to what’s included, which keeps your property organized and protected. Key points to remember about a revocable trust:

- You stay in control of your assets for as long as you’re able.

- You can change or cancel the trust at any time to fit your needs.

- Your trustee steps in only when needed, so the handover is clear.

When comparing a revocable living trust vs a last will, timing is the main difference. A trust takes effect while you’re alive and avoids probate. A last will applies only after death and must go through probate, which can delay asset distribution and make details public.

Living Trust vs Revocable Trust

A living trust can be revocable or irrevocable, depending on how much control you want to keep. A revocable trust may also be living or testamentary, but most people prefer a living one. It lets them stay flexible and make changes while they’re alive.

Who’s Involved in a Revocable Living Trust?

A revocable living trust involves several people who each play a specific role in managing and distributing assets.

- The grantor (also called the settlor or trustor) creates the trust and transfers money or property into it. Some grantors act as their own trustee while alive to keep control of their assets.

- The trustee manages the assets in the trust. They can be an individual, a family member, or a financial institution, and some people appoint co-trustees to share the responsibility.

- The successor trustee takes over if the original trustee dies, becomes disabled, or cannot continue, ensuring the trust continues without disruption.

- The beneficiaries receive the assets from the trust. The grantor may be the only beneficiary while alive or share this role with a spouse. After death, residuary beneficiaries receive what remains.

Clearly defining each role keeps everyone on the same page and makes it easier to manage the trust as life moves forward. It also helps avoid mix-ups or tension when it’s time to handle or pass on important assets.

Confirm a trust exists with a certificate of trust form.

Advantages of a Revocable Living Trust

A revocable living trust keeps you in control of your assets while you’re alive. If your preferences or circumstances shift, you can change or update the trust at any time. This estate planning form helps you avoid probate and keeps your estate details private. If you become incapacitated, your trustee can step in and manage your finances. Other key benefits include:

- Beneficiaries get access to assets right after death, without long delays.

- Transfers and updates stay simple, even as your finances or life change.

These features make a trust a practical way to manage your estate. It’s also easy to set up with Legal Templates’ revocable living trust template, helping you keep everything organized and in line with what you want.

Disadvantages of Revocable Living Trusts

A revocable living trust takes more work to set up and maintain than a will. You need to retitle your assets in the trust’s name and pay higher upfront costs. It doesn’t protect against creditors or taxes, and it needs ongoing attention to stay valid. Potential drawbacks include:

- Unfunded trusts cause problems and can leave some assets unprotected.

- You’ll still need a pour-over will to cover anything left out.

Understanding both sides helps you decide if a revocable living trust fits your long-term plans.

If you want another way to bypass probate, consider using an enhanced life estate deed if you live in Florida, Michigan, Texas, Vermont, or West Virginia.

When to Use a Revocable Living Trust

A revocable living trust fits best when you need flexible, long-term control over how your assets are managed and passed on. It’s especially useful when your life or finances are more complex and you want to make sure everything runs smoothly without court involvement. You may want to create one if any of these situations apply to you:

- You have dependents or aging parents who rely on you and need a clear plan for managing assets.

- You own property in multiple states and want one estate plan instead of several.

- You’re preparing for a long-term illness or incapacity and need someone you trust to manage your finances.

- You hold complex or high-value assets that require active management.

- You prefer to keep financial matters private and avoid court involvement.

If you own property in more than one state or want a simpler, more private way to handle your estate, a trust makes sure everything’s managed exactly how you want it. A revocable living trust helps you make sure your finances are managed the way you want, even if life takes an unexpected turn.

A revocable living trust is only one part of estate planning. Learn how it works with other key documents like wills, powers of attorney, and advance directives in our end-of-life documents guide.

How to Set Up a Revocable Trust

Once you know a revocable living trust is right for you, it’s time to put it in place. The setup is straightforward. You just need to decide who’s involved, what goes into the trust, and how you want your assets handled. Here’s how to do it.

- Decide who is creating the trust. Choose whether the revocable living trust is being set up by one person, a married couple, or two individuals working together.

- Name the grantor. Identify who’s putting property or funds into the revocable trust.

- Choose the trustee. This person manages the trust. You can serve as your own trustee, select someone else, or appoint co-trustees to share responsibilities.

- Appoint a successor trustee. Pick someone you trust to take over if the original trustee dies, becomes disabled, or steps down.

- Define the trustee’s powers. Decide how much authority the trustee will have. You can restrict certain powers or grant them authority under the Uniform Trust Code.

- Set compensation and bond requirements. Specify whether the trustee will receive payment and, if so, whether a bond is required for additional protection.

- List the property being transferred. Describe all assets going into the living revocable trust. Examples of assets you can put into a trust include bank accounts, investment accounts, real estate, and business interests. You can also include tangible personal property, including jewelry, collectibles, and artwork.

- Name the beneficiaries. List who will receive the assets and what percentage or share each one gets. If a minor will be the beneficiary of any assets in the trust, clearly specify how they will receive the property.

- Add special instructions. Include any specific gifts or wishes, like setting aside funds for a pet or donating to charity.

- Review the document. Make sure everything is correct and clearly reflects your intentions.

- Sign and notarize. This final step makes your revocable trust official and enforceable.

You don’t need to be wealthy to benefit from a revocable trust. It’s simply a smart way to keep your affairs clear, private, and stress-free. With everything mapped out, your estate is managed on your terms. Keep in mind there are different types of trusts, each built for a purpose—protecting assets, lowering taxes, or providing for family. The right one depends on what you want your trust to achieve.

Our recent study found that attorneys in the US typically charge $2,475 to create a revocable living trust.

State-Specific Trust Laws

Most states follow the Uniform Trust Code, which sets the rules for creating and updating living trusts and defines the rights of grantors and beneficiaries. Some states, however, add their own twists or separate laws. Check your state’s regulations below to make sure your trust meets all legal requirements.

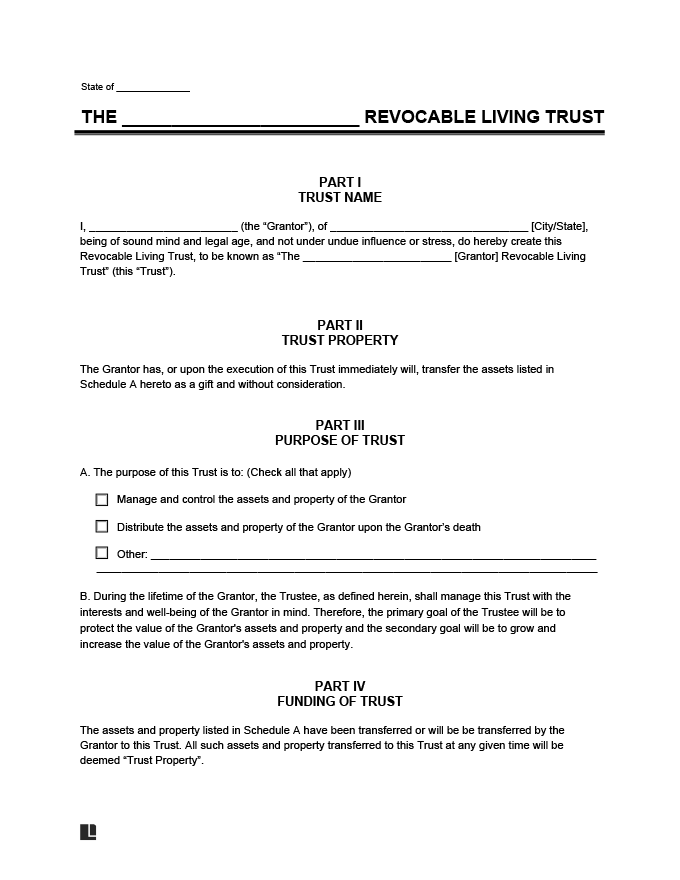

Sample Revocable Living Trust

View a sample revocable living trust to get a clear idea of how it’s structured. Then, download your free revocable living trust template in Word or PDF when you’re ready.