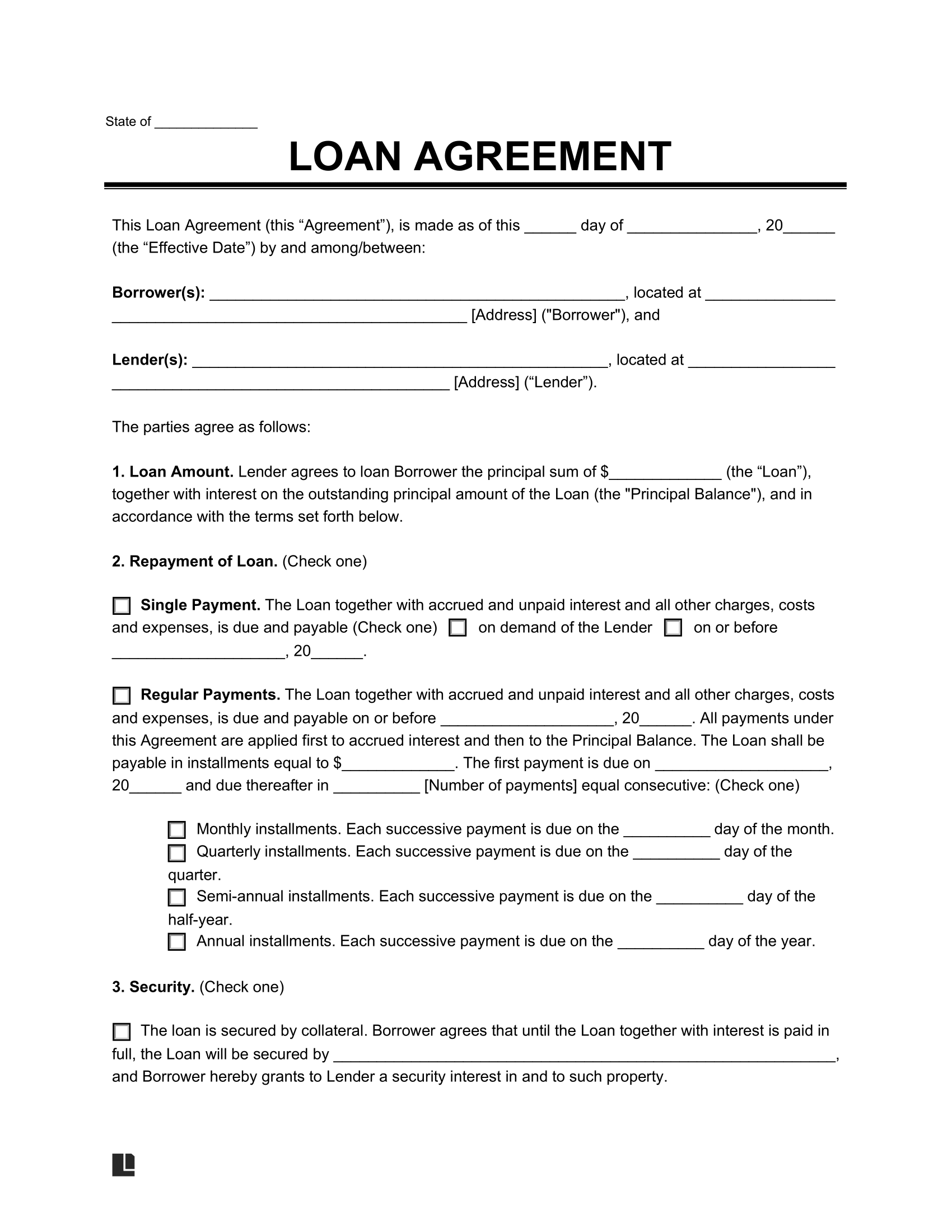

What Is a Loan Agreement?

A loan agreement is a legally binding contract between a borrower and a lender. It defines the repayment terms, interest, and fees, and protects both parties.

Writing a loan agreement shows that the transaction requires repayment and isn’t just a gift. If the borrower fails to pay the lender back, the document explains the consequences and provides legal recourse.

Loan Agreement vs. Promissory Note

A loan agreement and a promissory note serve similar purposes and both are legally enforceable, but the two documents include a few key differences. While both work to clarify loan repayment terms and interest rates, a loan agreement is more detailed and offers greater legal protections. Typically, more complex business or sales loans benefit from the detailed structure of a loan agreement.

A promissory note may be preferred for more straightforward deals, such as when the lender and borrower already know one another. Many people use a promissory note to set terms when lending to or borrowing from family members or friends.

| Factor | Loan Agreement | Promissory Note |

|---|---|---|

| Purpose | Formalizes loan terms. | Shows that borrower will repay the loan. |

| Parties Involved | Lenders, borrowers, and guarantors. | Lenders and borrowers. |

| Loan Types | Secured and unsecured loans. | Mostly unsecured loans. |

| Use Cases | Auto loans or complex personal loans. | Personal loans. |

Loan Agreements – By Type

You can customize the terms of your document depending on the type. Consider specific provisions for business loans, payment plans, or personal loan agreements. View our library of loan agreement templates to find the one that meets your specific purpose.

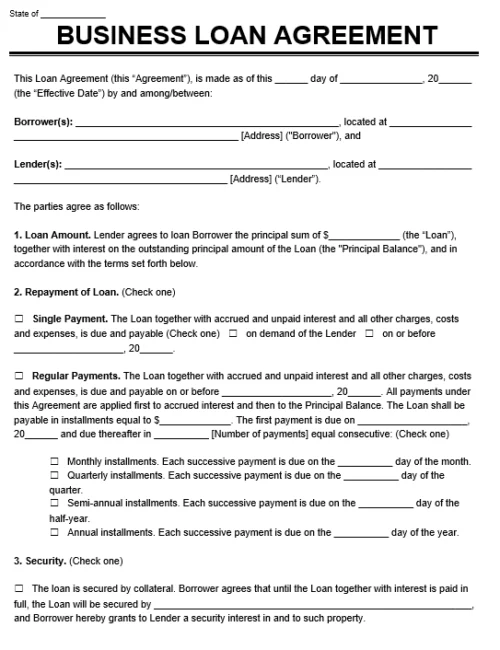

Outlines terms for lending money to a business, including repayment, interest, and collateral

Business Loan

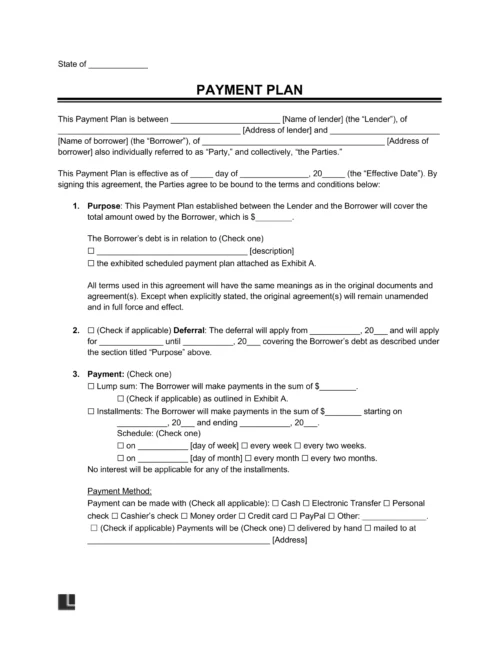

Establishes how a borrower will repay a debt in regular, scheduled payments

Payment Plan

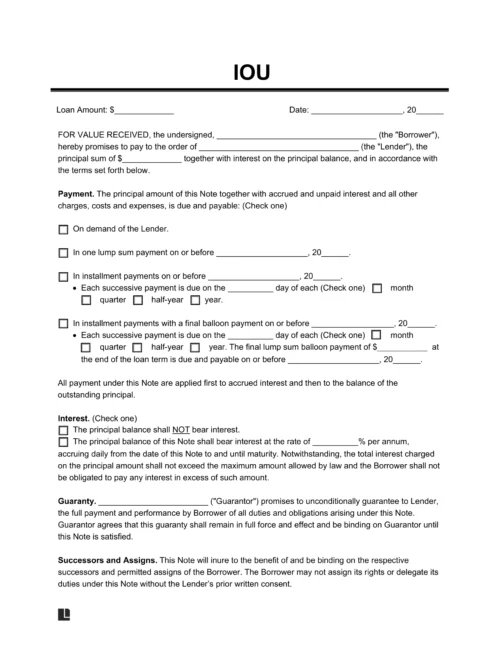

Acknowledges a debt in writing, including the amount owed and repayment expectations

I Owe You

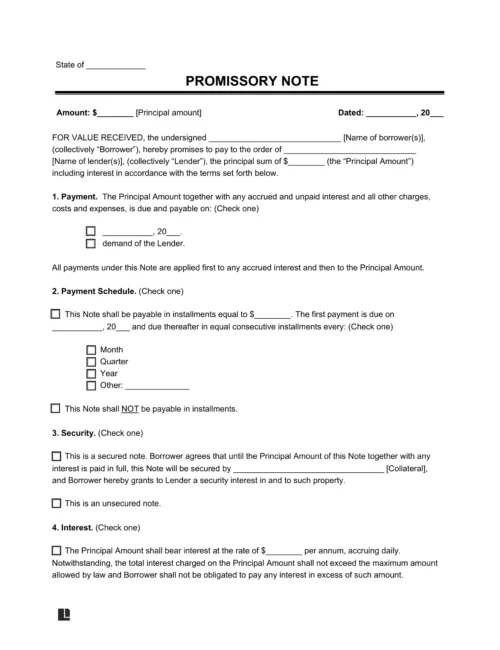

Legally documents a borrower's promise to repay a specific amount under agreed terms

Promissory Note

Formally forgives a borrower’s obligation to repay a loan or outstanding balance

Release of Debt

Provides legal security for a loan by placing property in trust until repayment

Deed of Trust

Grants a lender legal rights to property as collateral for a real estate loan

Mortgage Deed

When to Use a Loan Agreement

It’s best practice to have a loan agreement every time you lend or borrow money. While the terms may vary for each type of loan, having a written agreement offers extra protection and clarity. Create a contract for various situations, including the following:

- Personal loans for vacations, weddings, or medical situations

- Financial emergencies

- Auto purchases

- Mortgage or home renovations

- Educational expenses

How to Write a Loan Agreement

Your loan agreement’s language, format, and terms work to ensure fair and transparent conditions for everyone. Write an effective and binding contract with the following steps:

- State the date: Provide the full date for the agreement. This sets the timeframe for the execution of the agreement’s terms.

- Identify the lender: Clearly list the lender as an individual or a business entity. Provide the full legal name and address for this party.

- Name the borrower: Identify who is receiving the loan. State the full name of the individual or entity and include their address.

- Record the loan details: Record the exact loan amount, proposed repayment method, and applicable fees. Set the terms for due dates, late fees, and accepted payment formats.

- Outline the loan terms: Set the terms for the loan, such as the interest rates, collateral, default terms, and prepayments. Check state usury laws for maximum rates or other limitations when setting the interest rate.

- Set communication methods: Determine how the borrower and lender will communicate regarding payments, outstanding balances, or changes to the agreement. Typically, communication occurs through delivery services, registered mail, or email.

- Add a guarantor: If the lender wants an additional level of security, they may ask the borrower to add a guarantor to the agreement. The guarantor’s full legal name and contact information should be included, as this individual will be held responsible if the borrower defaults on payments.

- Determine conflict resolution: Set the governing state and method for disputes related to the agreement. All parties should agree to pursue arbitration, mediation, or litigation to handle conflicts or contract violations.

- Finalize and sign: Once all terms have been agreed upon, each party should sign the agreement to implement it.

Loan Agreement Sample

View the free loan agreement template from Legal Templates for more information about the formatting and terms to include. Our customizable loan agreement form allows you to add interest rates, fees, and payment conditions. Use our downloadable template, available in PDF and Word format, to define your loan terms.