Vehicle Bills of Sale – By State

Each state has different requirements for vehicle bills of sale. Differences include whether they are required, which parties must sign, and whether notarization is needed. Some states require bills of sale for specific vehicles, while others don’t. You may also find differences in what information you must include in the document.

Explore our state-specific guides for bills of sale. You’ll discover the exact requirements, the forms you must present at vehicle registration, and the associated fees.

- Alabama

- Alaska

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- District of Columbia

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming

What Is a Vehicle Bill of Sale?

A vehicle bill of sale is a legal document that records the sale of a car, motorcycle, or other vehicle. It proves the purchase and shows that the vehicle transferred ownership from the seller to the buyer.

This document serves as a type of sales agreement. It includes key information about the purchase, such as the date of sale, a vehicle description, and warranty details.

This document is especially important in private party transactions. It protects the buyer and seller in case disputes arise. Plus, it gives the buyer the proof they need to complete car registration and titling tasks.

Can You Register a Car With a Bill of Sale and No Title?

Once you buy a vehicle, you must often register it with your state’s Department of Motor Vehicles (DMV). In most cases, you cannot register a car with just a bill of sale and no title. If you have a bill of sale but not the title, you must use the bill of sale to apply for a bonded title. Alternatively, you may need to contact your state’s DMV for assistance. Find your state’s DMV office in the table below.

| State | Location | Bill of Sale Required? |

|---|---|---|

| Alabama | Vehicle Licensing Offices | Yes |

| Alaska | Division of Motor Vehicles | No |

| Arizona | Motor Vehicle Division | No |

| Arkansas | Department of Revenue Office | Yes |

| California | Department of Motor Vehicles | No |

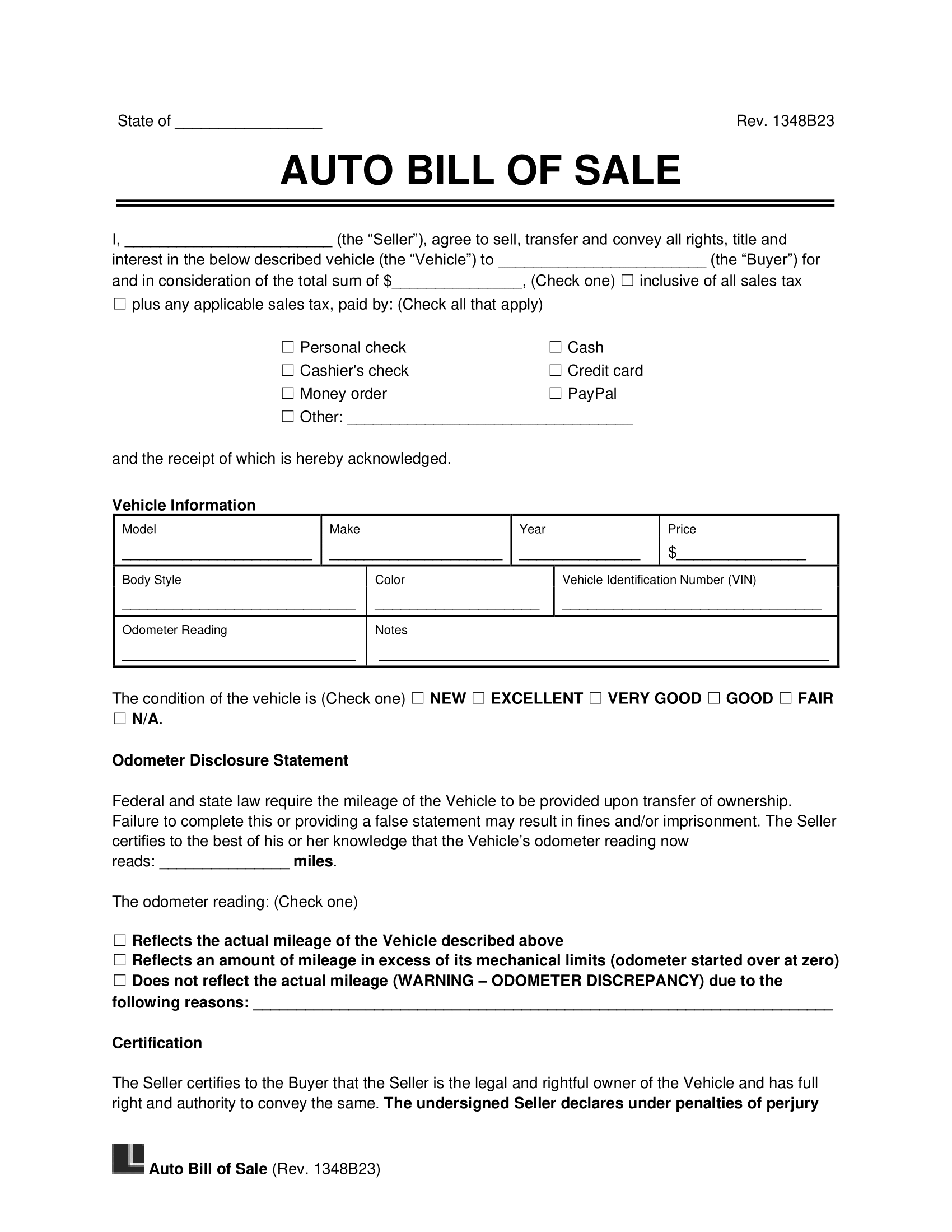

How to Write a Bill of Sale for a Car

Writing a bill of sale for a car helps prove the transaction occurred and identifies the new vehicle owner. Follow these steps and use Legal Templates’s form to write your own auto bill of sale.

Step 1 – Give the Date and Location of the Sale

Record the date that the parties will sign the bill of sale. Also, name the state where the car sale will take place. This distinction determines which state’s laws will govern the vehicle bill of sale.

Step 2 – List the Price & Payment Method

List how much the buyer will pay for the vehicle, and indicate whether the price includes sales tax. In most cases, the buyer must pay local and state sales taxes, but the seller may also be responsible if they profit from the vehicle sale. Typically, sales taxes are collected by the state DMV at the time the car is titled and registered in the buyer’s name.

Clarify what payment methods the buyer can use. When you use Legal Templates’s form, you can select from various options, including:

- PayPal

- Credit card

- Money order

- Cash

- Cashier’s check

- Personal check

Is the Car a Gift?

If the car owner is giving the car as a gift, use a gifted car bill of sale instead. This document shows it was a gift and provides proof for registration and titling.

Step 3 – Describe the Warranty

If the vehicle comes with a warranty, describe it in your auto bill of sale. New or used car bills of sale may provide some warranties, such as a promise to cover certain repairs for a specific period or amount of mileage.

Don't Want to Provide a Warranty?

If you don’t want to provide a warranty, make it clear that the car will come in its current condition with an as-is bill of sale.

Step 4 – Provide the Vehicle Information

Describe the vehicle in your car bill of sale, including its:

- Condition

- Vehicle identification number (VIN)

- Model

- Make

- Year

- Body style

- Color

- Any other disclosures that might be required by state law

Depending on the vehicle being sold, you may need to disclose its odometer reading. Per 49 CFR § 580.17, these vehicles are exempt from odometer disclosure requirements:

- Vehicles that weigh more than 16,000 pounds

- Vehicles that cannot move on their own (like trailers)

- Vehicles manufactured in or before the 2010 model year that are transferred at least 10 years after January 1 of the calendar year of their designated model year

- Vehicles manufactured in or after the 2011 model year that are transferred at least 20 years after January 1 of the calendar year of their designated model year

- Vehicles sold by the manufacturer directly to the US government

- Brand-new vehicles that haven’t been sold for personal or business use yet

Odometer Disclosure Statement

Discloses the current mileage of a vehicle.

Step 5 – Name the Buyer & Seller

Give the buyer’s and seller’s full names and addresses. This information establishes a clear record and helps the parties communicate with one another in case issues arise.

Step 6 – Sign & Notarize

Determine if you need a notary public to acknowledge your proof of vehicle sale. Some states require notarization, while others don’t. You may only need notarization under certain circumstances, like when the vehicle title is missing. Review your state’s requirements to determine if notary acknowledgment is needed.

Even if it’s not mandatory, having a notary public sign your vehicle bill of sale can add validity to the document.

Sample Vehicle Bill of Sale

If you’re wondering what a bill of sale looks like for a car, you can view a sample below. Complete our printable vehicle bill of sale when you’re ready. It’s also available to download as a PDF or Word file.

Other Types of Vehicle Bills of Sale

While a car bill of sale is common, your situation may require a different vehicle bill of sale. Explore our different templates below to find one that meets your needs.

Aircraft Bill of Sale

Lists important aircraft details and transfers ownership.

ATV Bill of Sale

Captures the essential ATV details and officially transfers the ATV to the buyer.

Bicycle Bill of Sale

Provides a record of the bicycle's specifics and legally passes ownership from the seller to the buyer.

Boat Bill of Sale

Lets you transfer ownership of a boat and document information about the watercraft.

Dirt Bike Bill of Sale

Details the dirt bike's information and finalizes the transfer of the vehicle from seller to purchaser.

Golf Cart Bill of Sale

Documents key specifications of the golf cart and legally shifts ownership from one party to another.

Jet Ski Bill of Sale

Outlines critical information about the jet ski and completes the sale by transferring ownership.

Mobile Home Bill of Sale

Logs important data about the mobile home and confirms the transfer of ownership between the parties.

Motorcycle Bill of Sale

Facilitates motorcycle transactions and allows you to transfer ownership from the seller to the buyer.

RV Bill of Sale

Provides a comprehensive record of the RV and facilitates the official change of ownership.

Scooter Bill of Sale

Contains important facts about the scooter while formalizing its handover from seller to buyer.

Semi-Truck Bill of Sale

Contains vital information about the semi-truck and legally transfers its ownership to the buyer.

Snowmobile Bill of Sale

Records the snowmobile’s specifications and facilitates the official transfer of ownership.

Tractor Bill of Sale

Ensures all necessary tractor details are documented while completing the transfer of ownership.

Trailer Bill of Sale

Helps convey ownership of a trailer to the buyer.

UTV Bill of Sale

Lists relevant details about the UTV and executes the transfer of title and ownership.